Market Commentary - September 2025

September 2025 Market Commentary

Overview

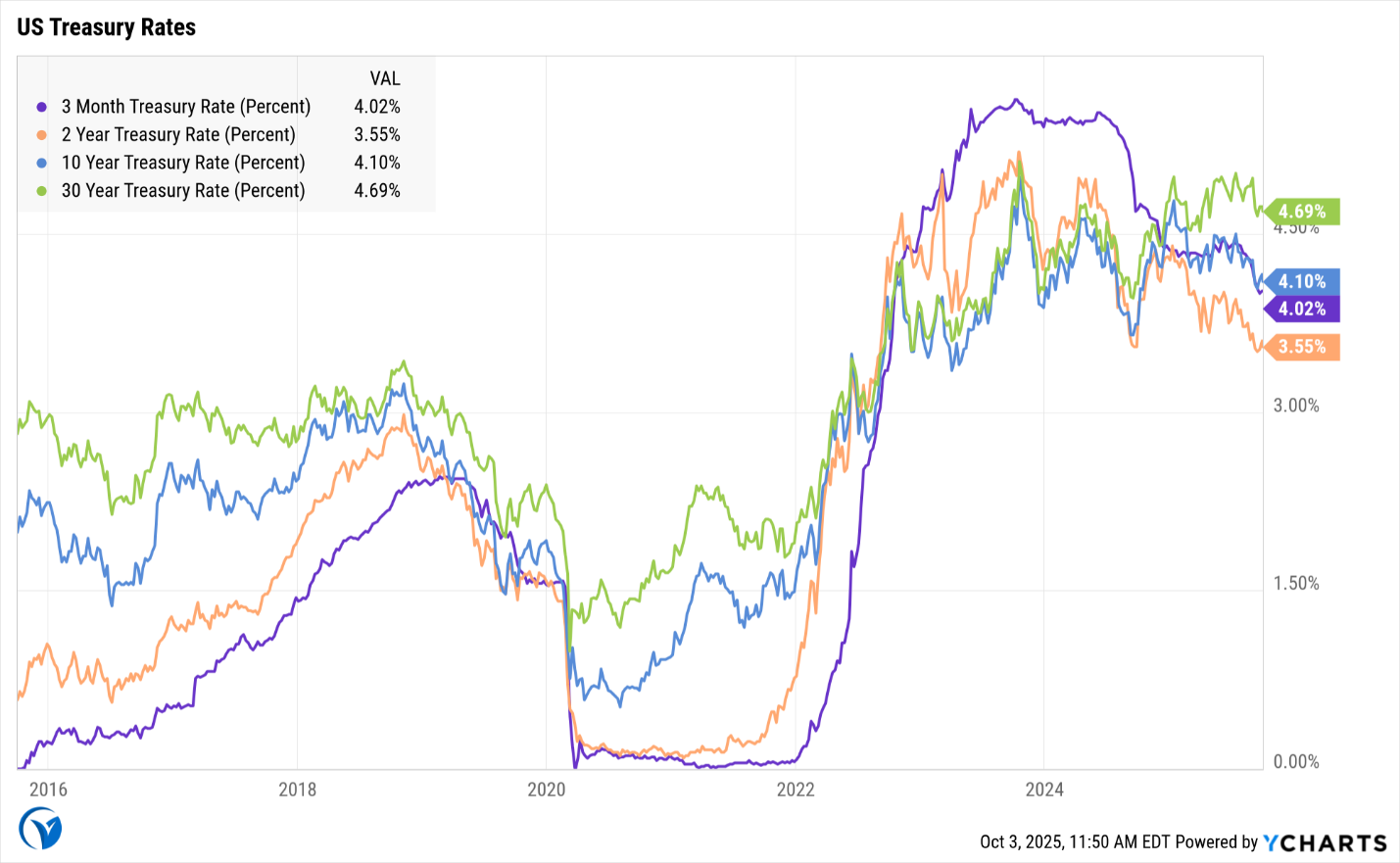

The Federal Reserve has officially initiated its easing cycle in response to intensifying economic challenges. Despite this policy shift, high equity valuations and persistent inflationary pressures suggest that investors should navigate this transitional period with caution. The September Federal Open Market Committee (FOMC) meeting marked a significant turning point, as the Fed reduced its benchmark interest rate by 25 basis points to a target range of 4.00-4.25%. This action represents the first rate cut of 2025. The decision comes as various economic forces converge , labor markets are deteriorating more rapidly than expected, inflation remains stubbornly above the Fed’s target—partly driven by increased tariffs—and stock valuations are at levels historically associated with market vulnerability. Chair Powell described the rate cut as motivated by “risk management” concerns rather than a shift toward aggressive easing.

Fed Pivots Toward Employment Concerns Amid Framework Overhaul

The central bank’s September rate cut was more than a routine policy adjustment; it occurred alongside the most significant revision to the Fed’s framework since 2020. The Fed eliminated its average targeting strategy and removed references to "employment shortfalls," indicating a return to a more balanced dual mandate. This position the Fed for what officials anticipate could be a period characterized by a higher neutral rate.

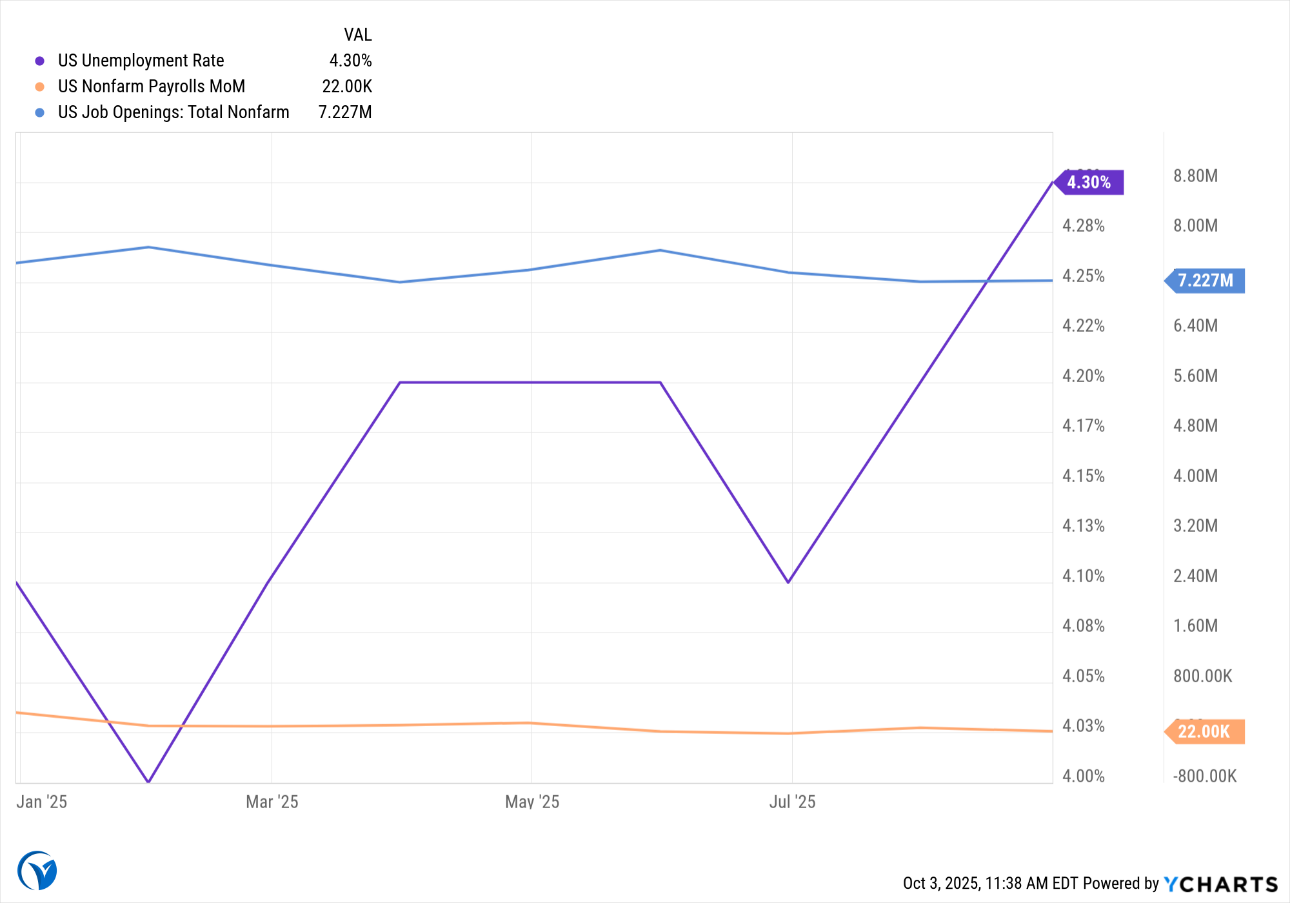

Chair Powell’s remarks at Jackson Hole and subsequent statements have underscored the Fed’s shifting priorities. With unemployment rising to 4.3% and average monthly job creation slowing to just 29,000 during the summer, policymakers are devoting increased attention to the weakening labor market. A substantial downward revision of 911,000 jobs for the twelve months ending March 2025 further highlights underlying economic fragility. Markets now expect two more quarter-point cuts before year-end, with fed funds futures pointing to a terminal rate of 3.50-3.75%.

Housing Market Shows Mixed Signals as Rates Decline

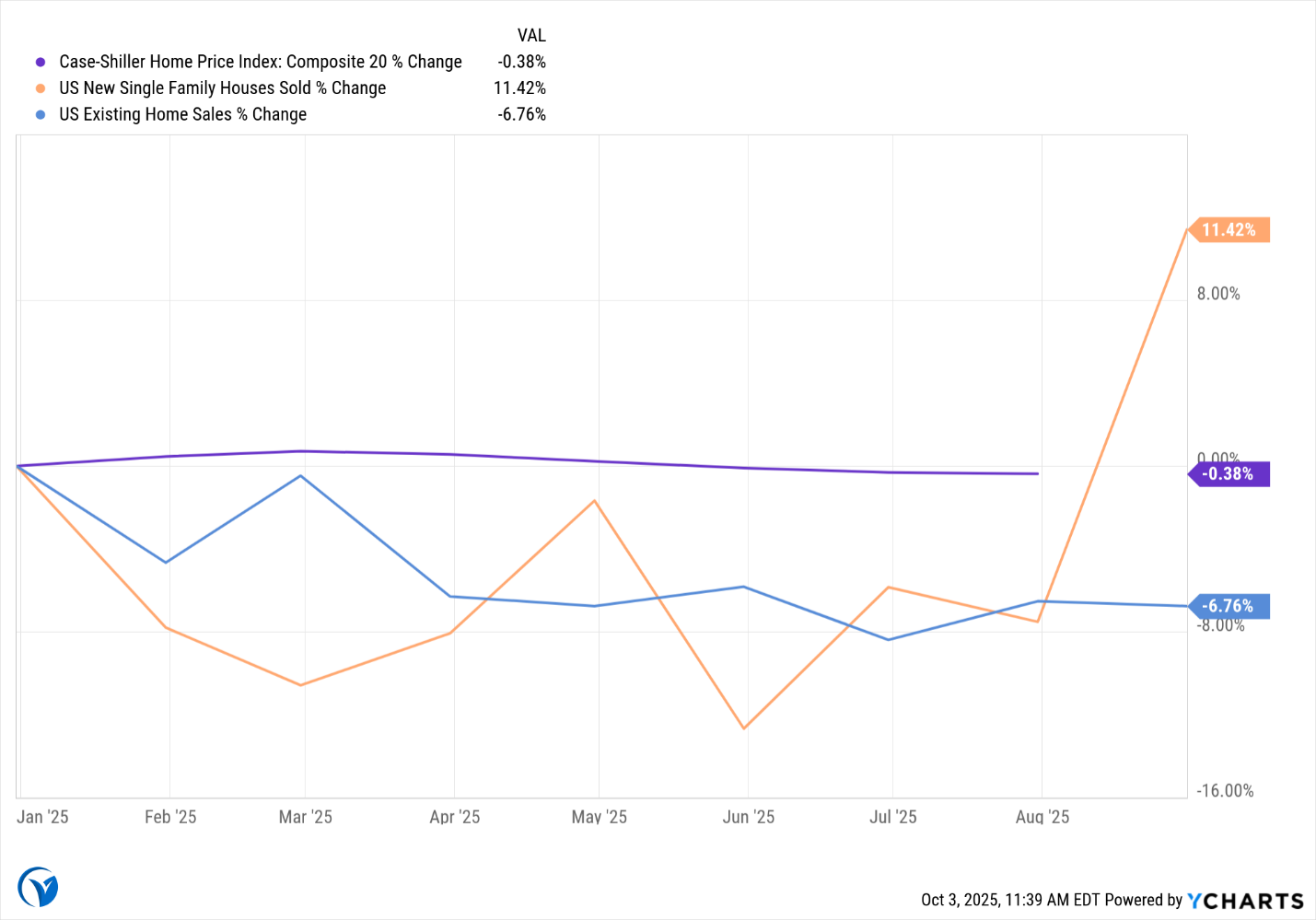

Mortgage rates have fallen to their lowest point since October 2024, with the 30-year fixed rate dropping to 6.39% in mid-September and refinancing applications surging by 58%. Nevertheless, the housing market faces ongoing challenges: existing home sales are running at an annual rate of 4.01 million, well below pre-pandemic levels.

Housing inventory has improved, climbing 15.7% year-over-year to 4.6 months of supply, marking the first substantial relief from supply constraints in years. Despite this, affordability is a persistent problem, as the typical mortgage payment now consumes over 35% of median household income. Regional disparities have become more pronounced, with Northeast markets showing relative resilience while Sun Belt regions experience price declines. In Florida, 85% of counties saw annual home price declines, and both Texas and California posted modest decreases after several years of growth.

The construction sector remains cautious. Housing starts fell by 8.5% in August to an annual rate of 1.307 million, reflecting builders’ hesitance to initiate new projects despite regulatory optimism under the current administration.

Tariff Pressures Drive Inflation Above Fed Comfort Zone

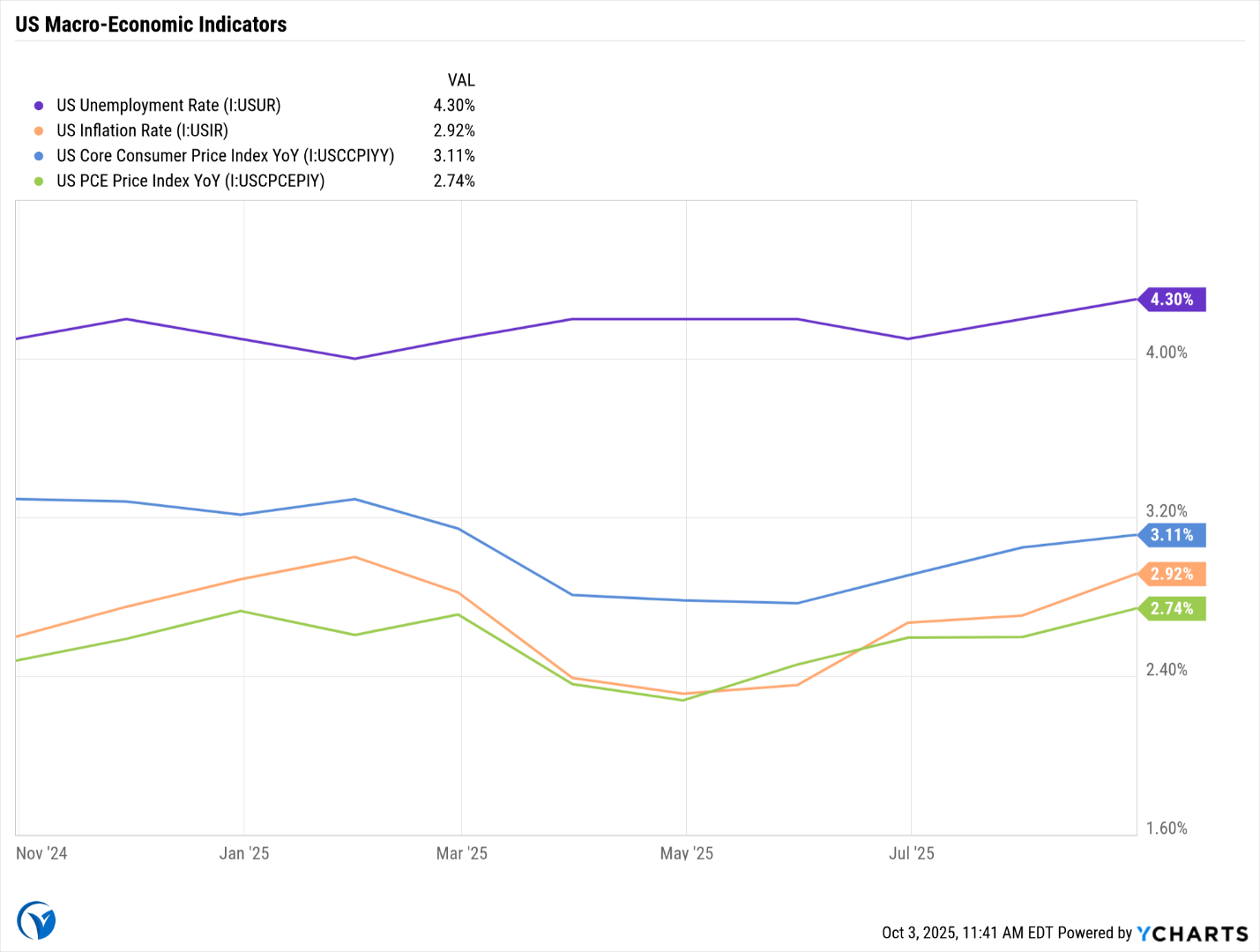

Inflation has become more complex due to the acceleration of tariff implementation throughout 2025. The August Consumer Price Index (CPI) rose to 2.9% year-over-year, with core CPI climbing to 3.1%, both exceeding July’s levels. The average effective tariff rate increased from 10% to over 23%, with early estimates suggesting these tariffs could add 1.0 to 1.5 percentage points to Personal Consumption Expenditures (PCE) inflation for the year.

Manufacturing input costs are escalating sharply, as shown by the ISM Prices Index reaching 63.7% in August. Business surveys report significant increases in commodity prices—including steel, aluminum, copper, and plastics—creating cost pressures that are beginning to impact consumers, though the full effects are still uncertain. Wage growth remains at 3.7% annually, providing real purchasing power gains but also contributing to persistent services inflation. The core PCE, the Fed’s preferred inflation measure, stood at 2.9% in July, remaining well above the 2% target that officials aim to reach by 2027.

Labor Market Deterioration Signals Broader Economic Cooling

Employment conditions have weakened considerably. August saw only 22,000 new jobs added—the slowest pace since December 2020—as the unemployment rate rose to 4.3%, signaling reduced hiring and stagnation in the labor market. Fed officials describe the current situation as “unusual,” with both labor supply and demand slowing simultaneously.

Major corporations have responded with significant cost-cutting measures. Intel announced 24,000 layoffs, marking its largest restructuring ever, while Microsoft, Oracle, Kroger, and Wells Fargo also implemented substantial workforce reductions. The DOGE initiative has resulted in over 200,000 federal workforce departures, with a target of 300,000 overall.

Consumer spending has remained relatively stable, with August retail sales rising 0.6% despite employment pressures. However, consumers are becoming more selective, prioritizing value and delaying discretionary purchases in anticipation of further tariff increases. Projections for holiday spending indicate a 5% decline compared to 2024.

Market Valuations Reach Concerning Extremes Despite Rate Relief

Stock markets are experiencing strong performance amid deteriorating fundamentals. The S&P 500 price-to-earnings ratio has climbed to 29.6–30.0, more than two standard deviations above historical averages and 80% above the modern-era mean of 20.5. This places valuations in "strongly overvalued" territory, a level that has historically preceded significant market corrections.

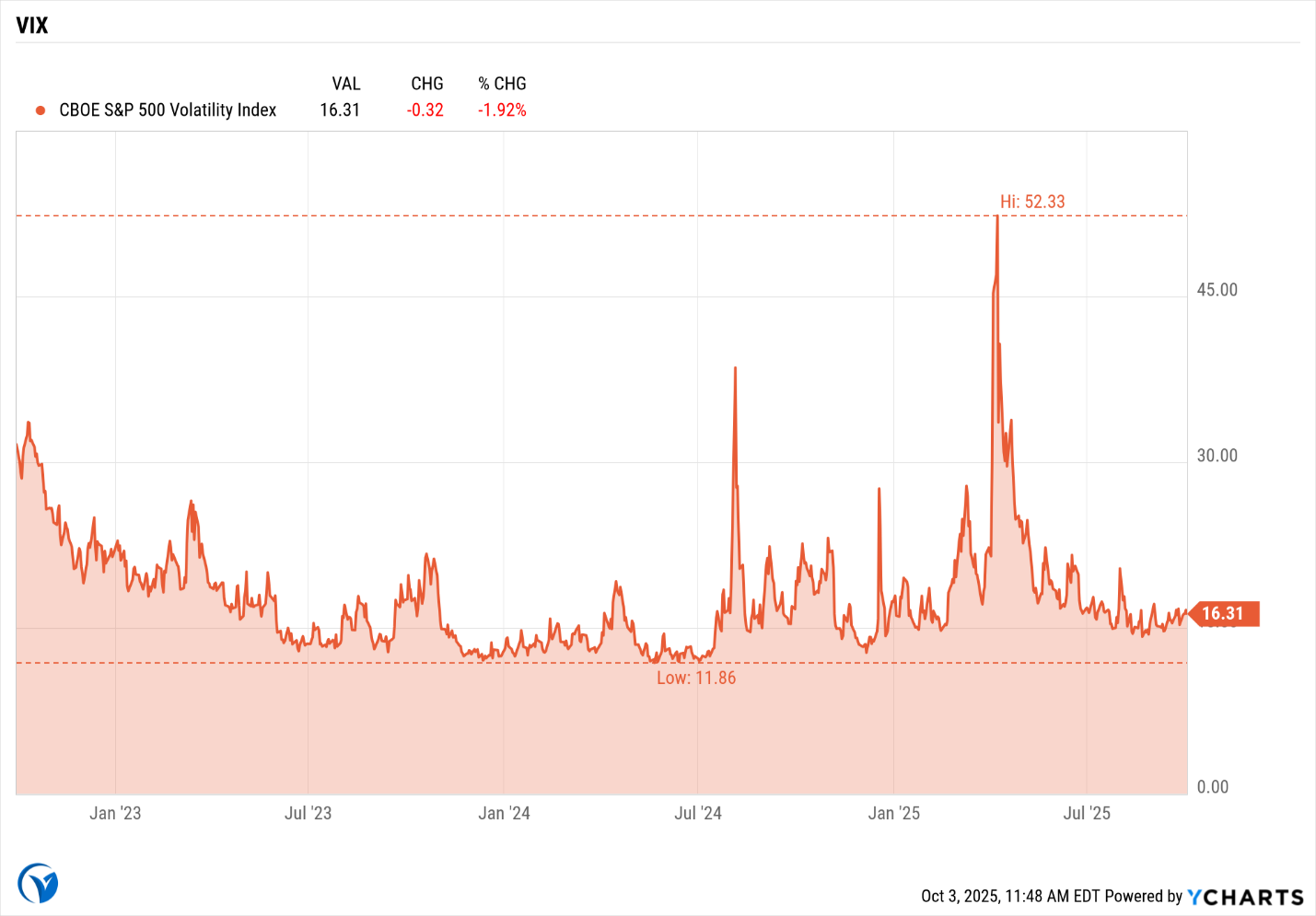

Technical indicators are signaling caution: The VIX remains subdued at 14.76, indicating complacency, while corporate bond spreads at 0.82% are near historic lows, reflecting compressed risk premiums across asset classes.

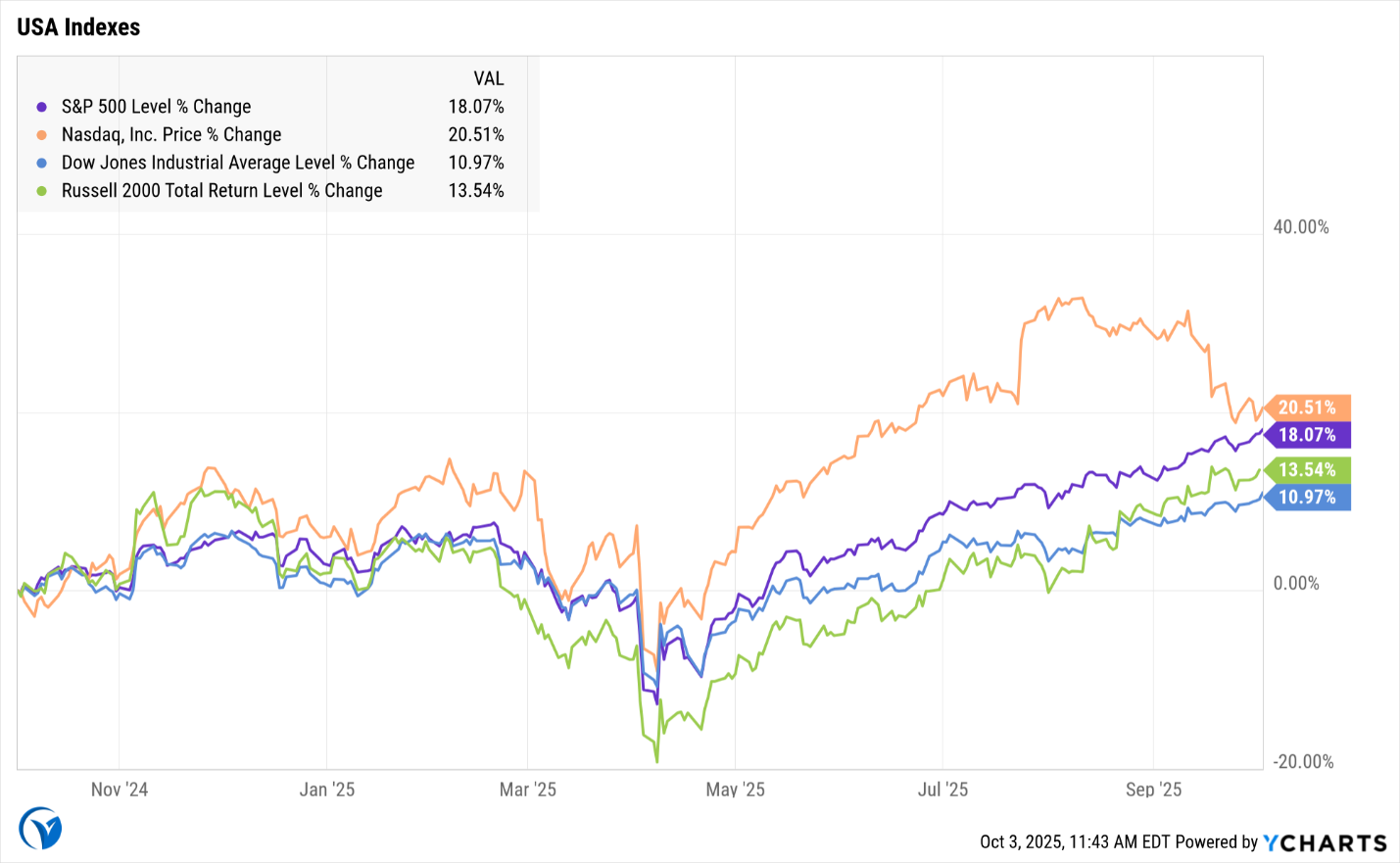

Despite these risks, markets have continued to rise, with the S&P 500 up roughly 30% since April and the Dow reaching new all-time highs above 46,000. The IPO market has experienced a revival, growing 76% in the first half of 2025, though the prevalence of SPACs—comprising 37% of new listings—points to speculative excess.

Government Shutdown and Implications

The government shutdown in 2025 has introduced additional uncertainty into the economic landscape, compounding existing concerns around inflation and labor market weakness. With key federal agencies operating at reduced capacity, delays in economic data releases and regulatory actions have made it more difficult for investors to gauge real-time market conditions. This lack of transparency can heighten market volatility and prompt risk aversion, especially as investors navigate an environment already marked by cost pressures and stretched valuations. Furthermore, the shutdown may delay fiscal policy responses and exacerbate the impact of tariff-driven inflation, making it essential for investors to closely monitor developments and adjust their portfolios accordingly.

Please do read our Vera Planning Whitepaper to delve deeper into the current Government shutdown. - System Under Strain: 2025 and the Unraveling of Federal Stability

Conclusion

September 2025 has brought markets to a pivotal juncture, where monetary policy accommodation intersects with economic deceleration and lingering inflationary pressures. While the Fed’s dovish approach provides short-term support, the combination of labor market weakness, tariff-driven cost pressures, and extreme valuations creates a precarious environment for further gains.

Investors should prepare for heightened volatility, as economic data may fall short of elevated expectations and policy uncertainties remain. Historically, markets trading at current valuation extremes are susceptible to corrections, particularly when economic momentum slows. Adopting defensive strategies and prudent risk management is advisable during this transitional phase.

Indices mentioned cannot be directly invested in. Securities offered through Registered Representatives of Cambridge Investment Research, Inc., a broker/dealer, member FINRA/SIPC. Advisory services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. Cambridge and VeranoviaOSJ, DBA Vera Planning, are not affiliated. The information in this email is confidential and is intended solely for the addressee. If you are not the intended addressee and have received this email in error, please reply to the sender to inform them of this fact. We cannot accept trade orders through email. Important letters, email, or fax messages should be confirmed by calling (678) 250-5099. This email service may not be monitored every day, or after normal business hours.

Key Market Indicies

.png)

.png)

.png)

.png)