July 2025 Market Commentary

As we navigate the mid-year landscape, the financial markets continue to present a dynamic interplay of opportunities and evolving regulatory frameworks. This month, our focus sharpens on three key areas that are significantly shaping investor strategies and the broader financial ecosystem: the persistent rise of Private Credit, the intricate and developing Digital Assets Laws, and the compelling discussion around the potential inclusion of Private Equity in 401(k) plans.

July has witnessed continued momentum in private credit, attracting substantial investor interest as a source of attractive risk-adjusted returns amidst a higher-for-longer interest rate environment. Concurrently, the digital asset space is undergoing a critical period of legislative evolution, with landmark bills such as the GENIUS Act and the CLARITY Act seeking to establish clearer regulatory boundaries and foster responsible innovation.

Finally, we delve into the ongoing debate about expanding access to private equity for retail investors through 401(k) plans, exploring both the potential benefits of diversification and enhanced returns, as well as the inherent risks and complexities involved. Read on to find out what these trends mean for your investments as we transition to the latter half of 2025.

Vera planning

Investment Committee and

Private Wealth Group

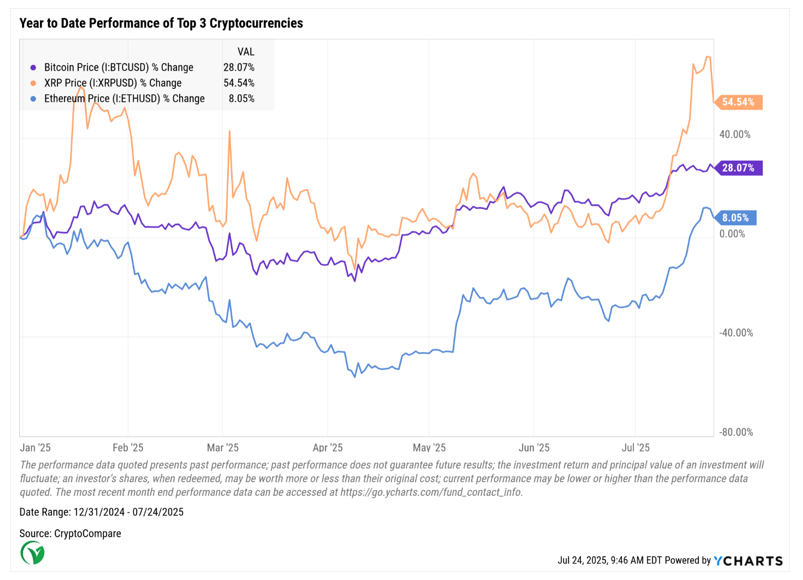

Digital Assets

The passage of the GENIUS Act and CLARITY Act marks a significant shift for US digital assets, moving from unclear regulations to a well-defined framework. The GENIUS Act sets strict rules for payment stablecoins, requiring them to be backed 1:1 by liquid assets like USD or Treasury obligations, and mandates regular audits and disclosures for consumer protection. These laws aim to strengthen the US dollar’s global position and attract investment by providing regulatory certainty.

The CLARITY Act sets clear roles for the SEC and CFTC in regulating digital assets by defining terms like “digital asset” and “digital commodity.” The CFTC will mainly oversee spot digital commodities, while the SEC will focus on anti-fraud and securities oversight. This act aims to reduce legal uncertainty, boost U.S. innovation and competitiveness, and align regulations with global standards to encourage domestic growth in digital assets.

New regulatory acts increase investor confidence through clearer rules and consumer protections but require retail investors to note key differences. Stablecoins, for example, lack federal deposit insurance even with strong reserves, unlike traditional bank deposits. Investor protections also differ: the CFTC oversees digital commodities with less stringent measures than the SEC provides for securities, which may result in varying safeguards across asset classes. Self-custody rights give investors direct control over assets but also more responsibility, as these funds do not have intermediary protections.

Complementing this legislative development, the emergence of spot Crypto Exchange-Traded Funds (ETFs) marks another major milestone in the mainstream adoption of digital assets. These investment products offer traditional investors regulated access to the underlying digital assets, such as Bitcoin, without the need for direct ownership or the complexities of self-custody. The approval of such products by regulatory agencies, especially the SEC, indicates a growing acceptance of digital assets within established financial markets and creates a new channel for institutional and retail capital to enter the sector. While providing benefits like liquidity, transparency, and ease of access, the performance of these ETFs remains inherently connected to the volatility of their underlying digital assets, requiring investors to stay vigilant and fully understand the associated market risks. The launch of these ETFs is expected to further democratize access to digital asset exposure, potentially expanding the investor base and supporting the overall growth of the digital asset ecosystem.

Bipartisan support signals broad agreement on regulating digital assets, with the aim of reestablishing US leadership in the sector and attracting capital and talent. Challenges persist—uncertain tax rules complicate compliance, and regulatory arbitrage remains a risk as firms may seek looser oversight by exploiting new definitions. Effective coordination between agencies like the SEC and CFTC, clear regulations, and industry adaptation are essential for moving from unregulated markets to an integrated digital finance system. Overall, this legislation marks a significant change in US policy, cementing digital assets in the financial landscape.

Private Equity in 401ks – The Good and the Bad

The inclusion of private equity in 401(k) retirement plans is emerging as a defining development in 2025. Traditionally limited to public stocks and bonds due to concerns around liquidity, transparency, and fiduciary duty, 401(k)s are now being reshaped by regulatory and industry shifts. The U.S. Department of Labor (DOL) has softened its stance, allowing fiduciaries to include private equity and crypto with proper due diligence—part of a broader effort to modernize retirement plan options.

Industry leaders like Empower have responded by launching professionally managed vehicles—including private equity, private credit, and real estate—accessible via collective investment trusts and advisor-managed accounts. These structures aim to democratize access to asset classes historically reserved for pensions and institutions.

Proponents highlight the strong long-term return potential of private equity, noting that over the past 20 years, it has delivered annualized returns of 14.3% compared to 8.1% for public equities . A 10% allocation to private equity could theoretically boost annual returns by approximately 50 basis points, potentially resulting in a retirement corpus that is 15% larger over 40 years . The American Investment Council further observes that private equity has outperformed public equities by 5–7% per year over the past decade. However, significant risks remain. Private equity funds are notably illiquid, often locking up participant funds for more than a decade, which complicates rebalancing and limits early withdrawals. High fees are another concern, with typical management fees ranging from 1.5% to 2% and performance fees at 20%, thereby reducing net returns. There is also the issue of valuation opacity and delayed pricing, which can obscure participants’ understanding of their account values. Finally, fiduciary liability is heightened for plan sponsors, as the Employee Retirement Income Security Act (ERISA) exposes them to increased litigation risk if investments underperform or lack sufficient transparency.

Recent market performance has also cooled enthusiasm. From Q2 2022 to Q2 2024, private equity returned just ~6.8%, underperforming the S&P 500’s ~12%, as rising rates and tighter credit weighed on deal-making. Prominent allocators like Yale’s endowment have trimmed exposure, while Senator Elizabeth Warren has raised questions about private fund transparency and suitability for retail investors.

Despite concerns, bipartisan support and new product structures are fueling cautious optimism. As of 2024, only 2.2% of 401(k) plans included alternatives, but this is expected to grow. Emerging solutions focus on limited allocations within diversified portfolios, guided by professional oversight to ensure suitability and compliance.

Ultimately, private equity’s integration into 401(k)s represents a bold shift—aimed at boosting long-term outcomes and closing the institutional-retail gap. But success hinges on gradual adoption, investor education, and regulatory clarity, ensuring innovation does not come at the expense of protection.

Private Credit and its Robust Growth

The past decade has been marked by the exponential growth of private credit markets, as an alternative to traditional bank loans or public debt. The size of this market has grown roughly five times since 2009, reaching nearly $2 trillion globally in 2024. Private credit offers the advantage of greater flexibility and customization since terms are negotiated directly between borrower and lender—usually institutional investors like asset management firms, pension funds, and insurance companies. Meanwhile, other tailwinds include the attractive yields offered by private credit opportunities and a continued retreat by traditional lenders due to regulatory constraints. Firms like Apollo Global Management, Ares, and Blackstone have been at the forefront of this expansion.

Intense competition because of the asset classes’ growth and a borrower-friendly credit environment has led to tighter spreads even as macroeconomic uncertainty and borrower leverage remain elevated. As spreads tighten, many borrowers are negotiating looser covenant packages and increasing their use of payment-in-kind (PIK) interest, which allows them to defer cash interest payments. This trend is worrying because it effectively pushes the repayment burden into the future, increasing the borrower’s debt load and potential for default. Deferred interest structures like PIK can also obscure a borrower’s true financial health, delaying recognition of distress.

As a result, questions and concerns arise over whether investors are being adequately compensated for the underlying credit risk, especially in deals with aggressive structures or limited financial transparency.

However, despite these risks, heightened competition, and tighter spreads, investor appetite remains robust. As a result, private credit managers are expanding to include new strategies and borrowers in asset-based finance, infrastructure financing, opportunistic credit, and commercial real estate lending spaces.

Meanwhile, the secondary market for private credit—long underdeveloped—is beginning to mature. Historically, the Private Credit market has been constrained by limited transparency and a lack of information available to investors. However, the market is now seeing increased activity in the GP-led secondary transactions market, which allows general partners to provide liquidity to limited partners without selling the underlying assets.

While still small in comparison to private equity secondaries, the private credit secondary market is gaining traction as investors seek greater flexibility and liquidity in an otherwise illiquid asset class. This evolution is expected to enhance transparency within the Private Credit market and offer new capabilities to portfolio managers across the industry.

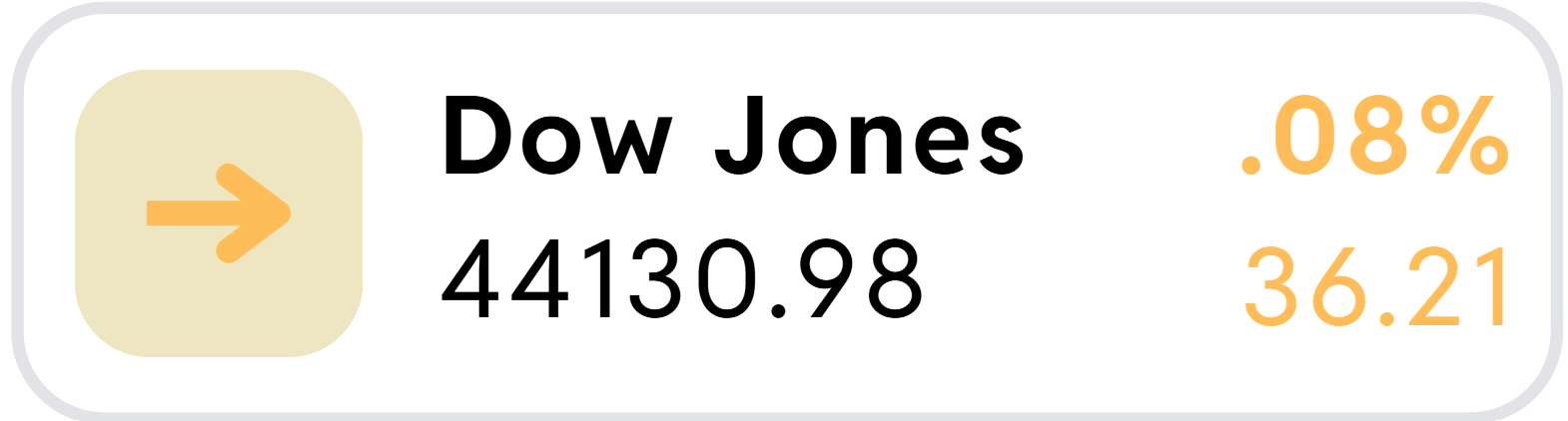

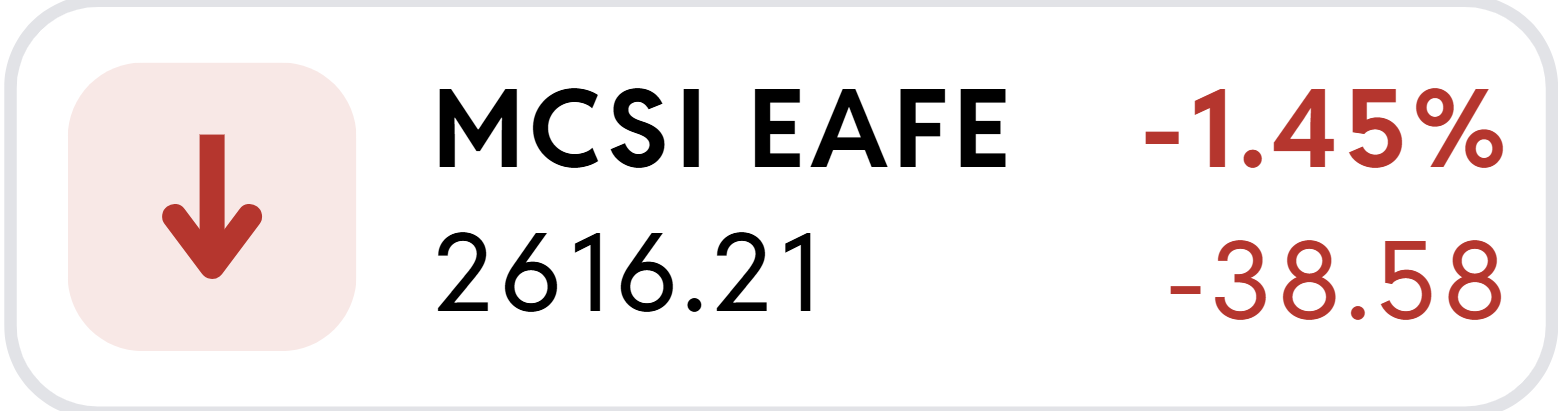

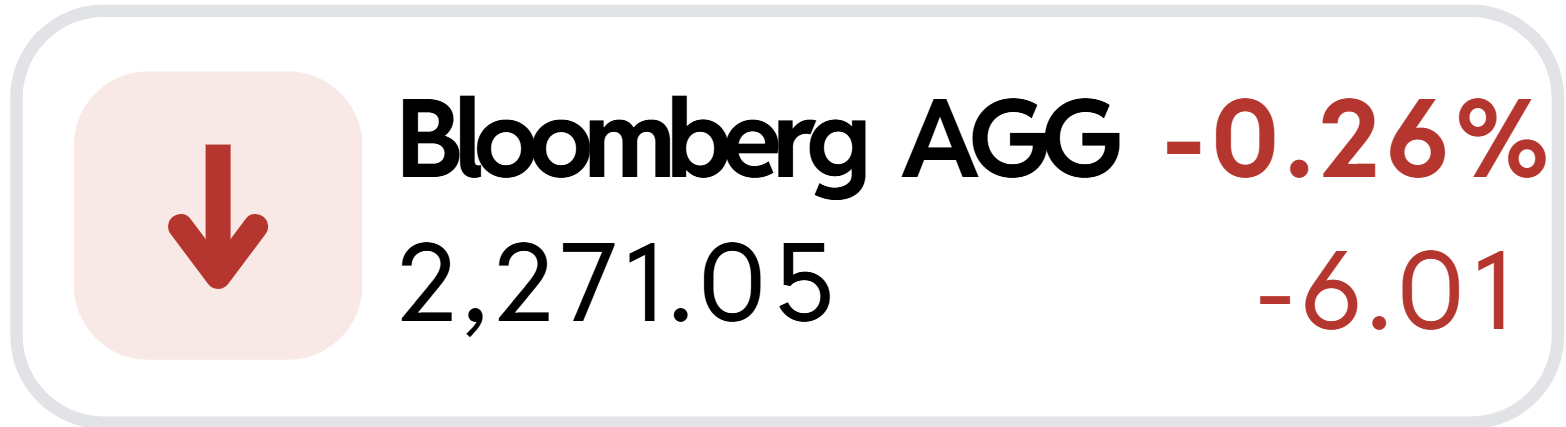

Key Market Indicies

*Market Indices as of 6/30/2025

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult a financial professional for your personal situation.

Past performance does not guarantee future results. Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Graphs provided by YCharts.

Key Market Indices according to Google Finance.

Securities offered through Registered Representatives of Cambridge Investment Research, Inc., a broker/dealer, member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. Cambridge and Vera Planning are not affiliated. The information in this email is confidential and is intended solely for the addressee. If you are not the intended addressee and have received this email in error, please reply to the sender to inform them of this fact. We cannot accept trade orders through email. Important letters, email, or fax messages should be confirmed by calling (678) 250-5099. This email service may not be monitored every day, or after normal business hours.