November 2025 Market Commentary

Our November market commentary aims to provide an overview of the key economic developments influencing financial markets and policy decisions in recent weeks. It explores the Federal Reserve’s ongoing challenges amid shifting labor market conditions, the impact of inflation on consumers and political outcomes, and the rapid growth of private credit markets. The analysis also delves into how investors and businesses are responding to heightened uncertainty, emphasizing the importance of focusing on economic fundamentals during periods of policy-driven volatility. We aim to provide insight into the current market volatility and share the knowledge and reasoning behind our Private Wealth Group Strategy.

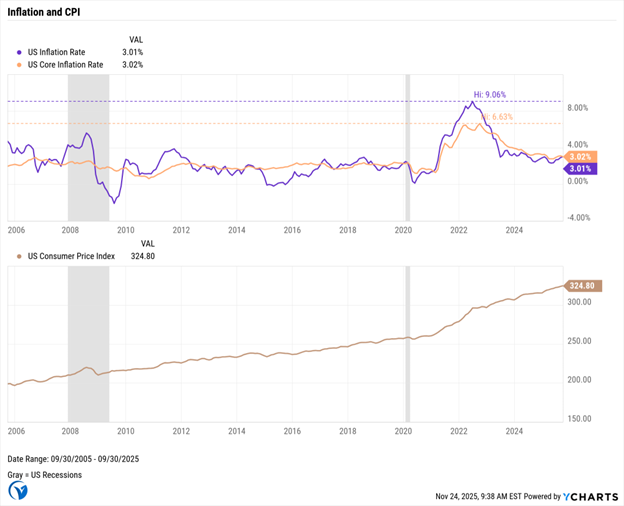

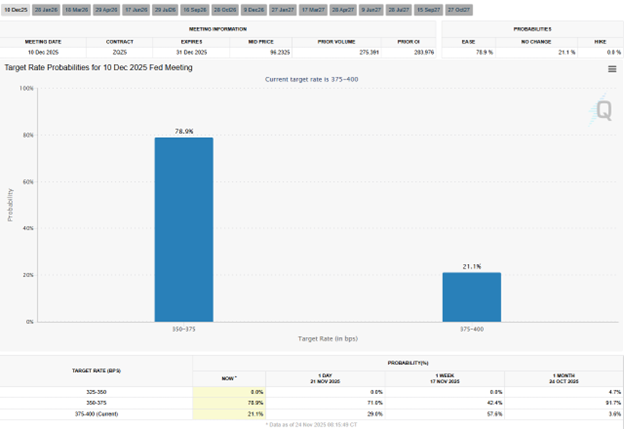

The government shutdown has complicated FOMC decision-making ahead of December. The October Consumer Price Index was canceled, and the Fed will not receive the November CPI or the November jobs report until several days after its meeting. Retail sales, trade figures, and the September jobs report — which already pointed to weaker labor-market conditions — were also significantly delayed, leaving policymakers to weigh policy with limited, lagged data.

Consumer Inflation

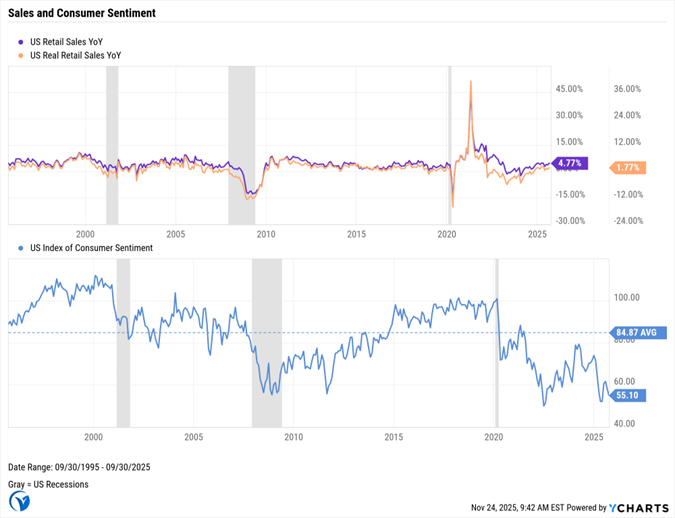

The issue of cost of living has been pulled to theforefront in the wake of high-profile Republican election losses. Voterfrustration over the cost of living impacted elections across Virginia, New Jersey, and New York. Chief among these developments was the election of ZohranMamdani as New York City mayor, on a platform that prioritized rental freezesand broader affordability measures like expanded tenant protections and freetransit. His victory, in the de facto heart of the American economy, highlightshow housing and affordability have emerged as defining issues for voters.

Tariffs have been a primary driver of recentinflationary pressures, with everyday staples such as coffee, bananas, andground beef hit especially hard. As of September, average retail prices forground roast coffee have surged more than 40% over the past year, while groundbeef and bananas have climbed 11.5% and 8.6%, respectively. Brazil—one of the largest suppliers of both beef and coffee to the U.S.—has been subject to 50%tariffs under the Trump Administration’s trade war, amplifying the cost burdenon consumers.

Prompted by the political fallout, the Trumpadministration has taken several actions to address rising prices:

· Rollback of select tariffs on items includingcoffee, beef, cocoa, and bananas

· Floating 50-year mortgages

· Agreements with pharmaceutical companies tolower prices

· Exploring $2000 tariff rebate checks toAmericans

However, supply-chains don’t necessarily reactquickly and it could be a long-time before tariff-reduced inflation clears.

Private Credit

The private credit market has surged, driven bycompanies seeking the flexibility of non‑bank financing and institutionalinvestors eager to capture its elevated yields. The recent bankruptcies of auto‑partssupplier First Brands and subprime auto lender Tricolor Holdings have drawnscrutiny to the underwriting practices of direct lenders, raising concernsabout credit quality and the potential for broader impacts across leveragedfinance markets. The private credit arms of high‑profile firms such asJefferies, UBS, and Millennium were left with more than $10 billion in loan exposure toFirst Brands — a burden that has already translated into significant losses,even though some recovery remains possible.

Industry leaders remain divided over whether these developments signal deeper trouble for private credit markets. Jamie Dimon, commenting on the Tricolor and First Brands bankruptcies, warned, “When you see one cockroach, there’s probably more,” after JPMorgan took a $170 million impairment tied to Tricolor. Some private credit executives bristled at there mark, rejecting the idea that systemic issues are at play. Yet as privatecredit has surged in popularity, lenders have increasingly loosened terms to winbusiness—embracing more flexible covenants and payment‑in‑kindstructures that heighten risk in the pursuit of yield.

Private capital has unlocked significant fundingand stepped in to fill a void that traditional bank loans and public bondscould not. Overall, this may represent a positive development, offeringcompanies greater flexibility and investors new opportunities. At the same time, it reflects a broader shift toward non‑public lending. While thisflexibility has fueled rapid growth, it also raises concerns abouttransparency, investor protections, and the resilience of the system as privatecredit continues to expand and mature.

The private credit market has surged, driven by companies seeking the flexibility of non‑bank financing and institutional investors eager to capture its elevated yields. The recent bankruptcies of auto‑parts supplier First Brands and subprime auto lender Tricolor Holdings have drawn scrutiny to the underwriting practices of direct lenders, raising concerns about credit quality and the potential for broader impacts across leveraged finance markets. The private credit arms of high‑profile firms such as Jefferies, UBS, and Millennium were left with more than $10 billion in loan exposure to First Brands — a burden that has already translated into significant losses, even though some recovery remains possible.

Industry leaders remain divided over whether these developments signal deeper trouble for private credit markets. Jamie Dimon, commenting on the Tricolor and First Brands bankruptcies, warned, “When you see one cockroach, there’s probably more,” after JPMorgan took a $170 millionimpairment tied to Tricolor. Some private credit executives bristled at theremark, rejecting the idea that systemic issues are at play. Yet as privatecredit has surged in popularity, lenders have increasingly loosened terms to winbusiness—embracing more flexible covenants and payment‑in‑kindstructures that heighten risk in the pursuit of yield.

Private capital has unlocked significant fundingand stepped in to fill a void that traditional bank loans and public bondscould not. Overall, this may represent a positive development, offeringcompanies greater flexibility and investors new opportunities. At the sametime, it reflects a broader shift toward non‑public lending. While thisflexibility has fueled rapid growth, it also raises concerns abouttransparency, investor protections, and the resilience of the system as privatecredit continues to expand and mature.

Focused on Fundamentals Amidst Policy Fluctuations

The recent surge in market volatility is largelyattributable to the ongoing uncertainty surrounding the Federal Reserve'sfuture interest rate policy and the sticky nature of inflation. As centralbanks carefully navigate the path to price stability, investors have beenclosely scrutinizing every piece of economic data—from employment numbers toinflation reports—which leads to sharp, temporary market swings as expectationsfor future rate cuts shift. While it is true that elevated interest rates increaseborrowing costs for both consumers and businesses, our confidence remains highbecause the underlying economy and corporate sector have shown remarkableresilience. We are seeing a broadening of corporate earnings growth beyond thelargest technology companies, which signals a healthy adaptation by businessesto the current cost environment. This fundamental strength acts as a powerfulcounterbalance to policy-driven volatility.

This period of fluctuation is therefore not a sign of fundamental weakness, but rather a necessary re-pricing exercise. Higherrates simply mean investors require a greater return for the risk they take,and volatility creates opportunities for us to enhance portfolio positioning.The key is to look past the daily noise and focus on the long-term innovationand productivity gains that continue to fuel economic progress, particularly inforward-looking sectors like technology and digitalization. The history ofmarkets has taught us that patience and discipline are the greatest assetsduring periods of stress. By maintaining a diversified and deliberate strategy,we are positioned to capitalize on attractive valuations that emerge from thecurrent policy debate, ensuring your portfolio remains squarely focused on thesubstantial compounding opportunities that the future holds. We believe thecurrent policy-induced turbulence will ultimately give way to a clearereconomic path, making this an excellent time to remain steadfastly invested.

Securities offered through Registered Representatives of Cambridge Investment Research, Inc., a broker/dealer, member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. Cambridge and Vera Planning are not affiliated. The information in this email is confidential and is intended solely for the addressee. If you are not the intended addressee and have received this email in error, please reply to the sender to inform them of this fact. We cannot accept trade orders through email. Important letters, email, or fax messages should be confirmed by calling (678) 250-5099. This email service may not be monitored every day, or after normal business hours.

These are the opinions of [rep/author name] and not necessarily those of Cambridge, are for informational purposes only, and should not be construed or acted upon as individualized investment advice. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is not a guarantee of future results.