May 2026 Market Commentary

May 2026 Market Commentary

Introduction

May 2026 was marked by exceptional market volatility as seasonal investing patterns collided with major geopolitical disruptions and an unusually large capital-spending cycle. The familiar Wall Street saying, "Sell in May and go away," has not applied this year. Instead, supply-driven energy shocks and escalating conflict in the Middle East have reignited inflation concerns, while a powerful structural wave of AI investment has helped support global equity markets.

Three themes now dominate market positioning: renewed inflation pressure, intensifying geopolitical risk, and the continued expansion of AI-led capital spending. Together, these forces are shaping asset allocation, risk premiums, and expectations for global monetary policy.

Macro & Inflation: The Energy-Driven Pricing Resurgence

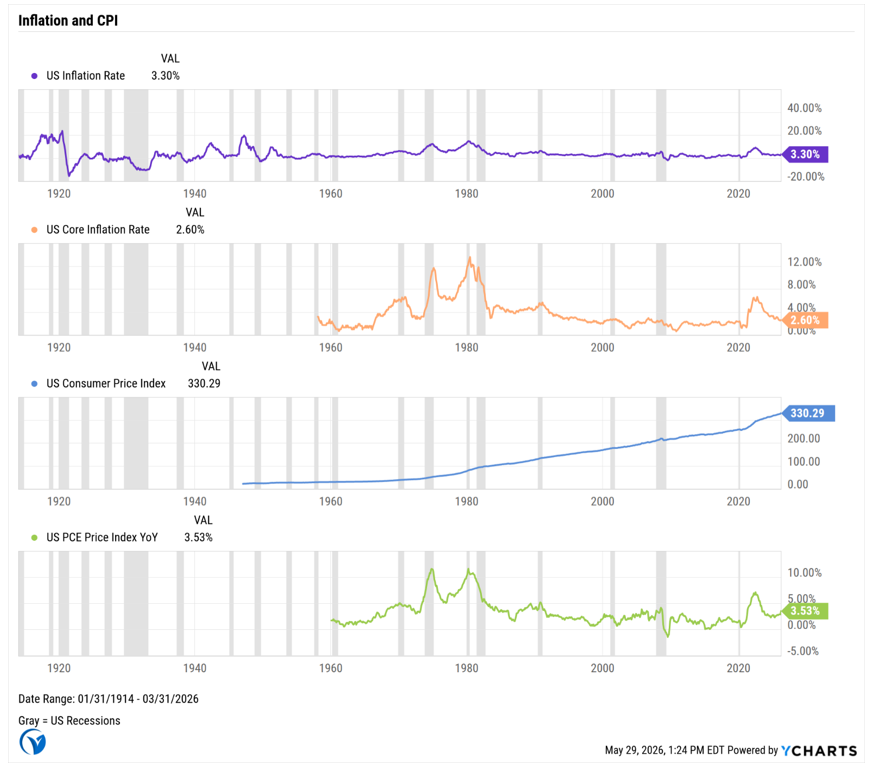

Inflation has re-emerged as the most immediate challenge for central banks, undermining expectations of a smooth late-cycle return to target.

The late-May release of the Personal Consumption Expenditures (PCE) price index which is the Federal Reserve’s preferred inflation gauge solidified the Fed Stance on Interest Rates. Year-over-year PCE inflation for April rose to 3.8%, up from 3.5% in March, marking the fastest pace of acceleration in three years. On a month-over-monthbasis, PCE increased by 0.4%.

The primary driver of this rebound is the direct transmission of higher energy costs into the broader economy. Retail gasoline prices rose 5.5% month over month, bringing the average U.S. gallon to $4.42, up sharply from $2.98 in late February. Food prices also increased by 0.5% as logistics and fertilizer supply chains came under strain.

Rising prices alongside slowing growth are reviving concern about a stagflationary backdrop. That combination has pushed bond markets to reassess the path of Federal Reserve policy and has added pressure to yields ahead of the June meeting.

Geopolitics: The Iran Conflict and the Hormuz Bottleneck

Geopolitical risk has moved from a tail risk to a core market variable, reshaping trade flows and global energy pricing.

Joint military operations that began in late February eased on May 5, but the political and economic fallout remains significant. By late May, negotiations in Islamabad and diplomatic channels in Oman had produced a tentative memorandum of understanding for a 60-day ceasefire extension.

The Strait of Hormuz remains the key bottleneck for global trade. Disruptions and localized blockades have materially reduced crude and liquefied natural gas (LNG) shipments, prompting threats of sanctions from the U.S. Treasury against regional intermediaries.

Oil prices have become a real-time measure of ceasefire expectations. After earlier conflict-driven highs, Brent crude eased to roughly $93 per barrel and WTI traded just below $88 on hopes of a diplomatic breakthrough. Any sign that the 60-day truce could fail or reports of violations such as intercepted missile events near Kuwait could quickly restore a $5 to $10 risk premium to energy futures.

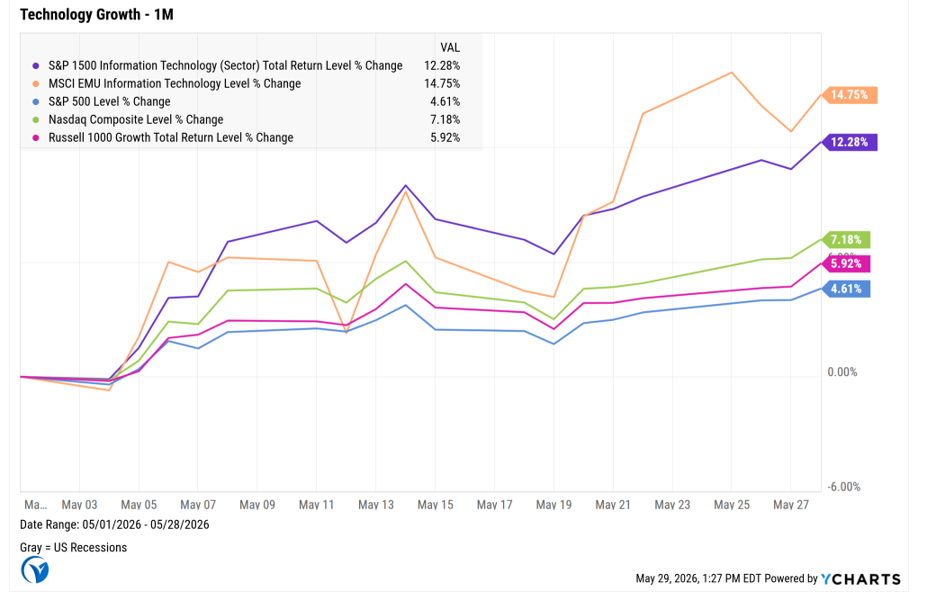

Tech & Growth: The $700 Billion AI Trade Reshapes the Index

Despite higher yields and energy costs, equity benchmarks have avoided a deeper correction. The main support has been the large, non-discretionary capital-spending cycle led by technology hyperscalers.

The 2026 Global Tech Landscape

Tech companies have offered guidance to approximately $700 billion in total 2026 capex, with an estimated 75% directed toward physical AI infrastructure.

Market attention has shifted from demand to execution risk. The main areas of concern are hardware reliability and failure rates in million-chip clusters, bandwidth constraintsin inter-chip communication and optical networking, and power-grid limits paired with rising cooling requirements.

Microsoft, Alphabet, Meta, and Amazon are driving this spending wave. Because the investment is structural rather than cyclical, it has remained resilient even amid macro softness and has helped offset the usual seasonal weakness associated with "Sell in May."

While Nvidia and other chip designers remain central, investor attention is broadening toward the infrastructure and execution bottlenecks required to scale AI effectively. Networking bottlenecks are becoming more important as clusters expand to extremely high chip densities and internal data traffic leaves processors waiting for data. At the same time, power generation, grid connectivity, and cooling capacity are emerging as key constraints in the AI buildout, making utilities and clean-energy providers more important to the broader investment theme. Investors are also increasingly looking beyond hardware leaders toward IT consulting and management firms that help enterprises implement AI.

Conclusion

To conclude, these developments suggest a market environment that remains difficult to read with confidence. Inflation pressures, geopolitical uncertainty, and the ongoing AI investment cycle continue to pull markets in different directions, leaving the near-termpath less than clear. For now, the balance between risk and opportunity may depend less on a single dominant narrative and more on how these market forces evolve in relation to one another over the coming months.

Disclosure: This piece is not intended as investment advice and has not been tailored to any specific individual's situation. It is for informational purposes only.