March 2026 Market Commentary

March 2026 Market Commentary

Overview

March marked a decisive break from the data driven calm of early 2026. Instead, markets were forced to digest a rapidly escalating geopolitical crisis,mounting stress in private credit, and a renewed surge in inflation expectations. The result was broad based volatility across equities, fixed income, and credit as investors reassessed both the durability of the expansion and the Federal Reserve’s path forward.

Private Credit Stress

Stress in private credit shifted from isolated incidents to a broader confidence shock. Early concerns stemmed from the 2025 bankruptcies of First Brands Groupand Tricolor Holdings, which raised questions about underwriting standards. February’s sharp sell-off in technology and software stocks added a newdimension, as investors began to reassess the durability of Saas-backedlending. Fears that AI could compress traditional Saas revenue models prompted lenders to revisit valuations and, in some cases, mark down assets.

Several high-profile redemption restrictions underscored the fragility of the asset class:

- Morgan Stanley limited withdrawals after investors attempted to redeem nearly 11% of shares in one fund

- BlackRock restricted redemptions in its HPS Corporate Lending Fund (HLEND)

- Blue Owl Capital continued to unwind the fallout from its February sale of $1.4 billion in assets and the permanent suspension of redemptions in one ehicle

- Cliff water capped repurchases at 7% after requests reached 14%.

- JPMorgan marked down certain private credit linked loans, signaling reduced willingness to extend financing to the sector

- Apollo Global Management capped withdrawals at 5% of outstanding shares after clients sought to redeem over 11% in its $25B Apollo Debt Solutions business development company

These developments reinforced a growing concern about the rapid expansion of private credit and a mismatch between when investors want their capital back and the duration of loans. March marked one of the first times this mismatch became systematic, forcing a broad repricing of private-market risk and raising deeper questions about valuation transparency, fund structure, and the sustainability of the sector’s rapid growth.

Energy Shock and the Iran Conflict

On February 28, 2026, the U.S. and Israel launched surprise military operations against Iran amid escalating tensions over Iran’s nuclear program and its support for groups such as Hezbollah and Hamas. The strike killed several high-ranking Iranian officials, including the Supreme Leader. The conflict intensified throughout March as Iran retaliated with drone and missile attacks, sending shockwaves through global energy markets and disrupting key supply chains. European NATO members resisted U.S. calls for deeper involvement, focusing instead on the economic fallout. The lack of unified Western engagement has added to market uncertainty.

Strait of Hormuz, Regional Impact, and Helium Supply

The partial blockage of the Strait of Hormuz - a transit route for one-fifth of global oil, left hundreds of ships stranded. Even a temporary disruption has outsized consequences for global energy supply, shipping costs, and inflation expectations.

Furthermore, the conflict spilled into neighboring countries, damaging key Oil & Gas facilities:

- Qatar’s Ras Laffan Industrial City, the world’s largest LNG facility, suffered damage that could eliminate 17% of global LNG capacity for years

- Kuwait’s largest refinery was hit by drone attacks

- Oman’s Port of Salalah .an essential fallback route for shipping avoiding Hormuz was struck, disrupting container flows across Asia, East Africa, and the Gulf

Qatar’s Ras Laffan facility also produces more than 1/3 of global helium, a critical input for semiconductors, medical imaging, aerospace, and scientific research. Damage to the facility raised concerns about a helium shortage.

Energy Market Impact

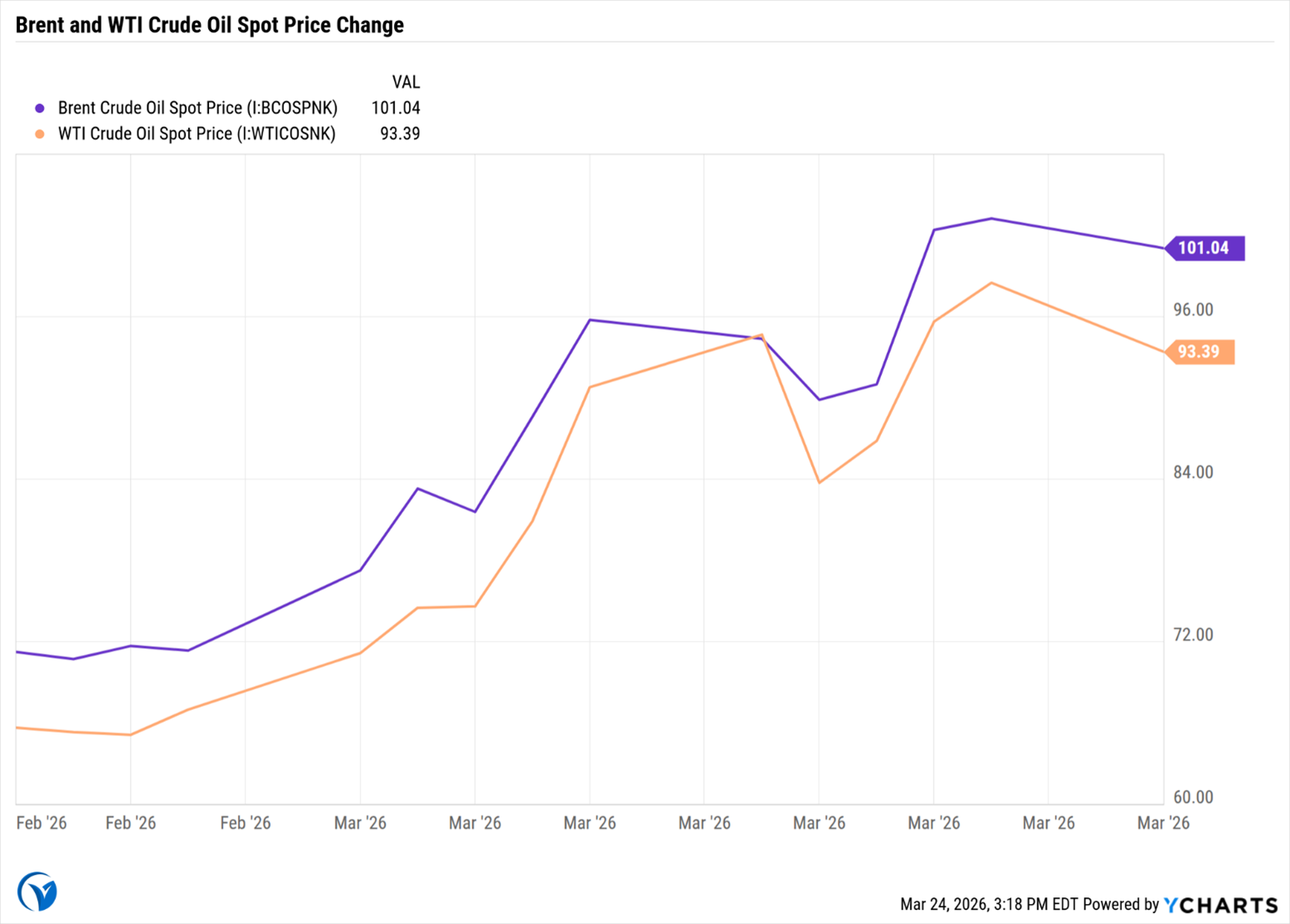

Brent crude surged past $100/bbl to a high of $112/bbl on March 12, up from approx. $70 before the conflict. U.S. gasoline prices climbed to $3.84 per gallon by March 18, compared with $2.98 before the late February strikes.

At first, markets appeared to be pricing in a short conflict, but the physical disruptions point to a longer lasting shock. War related energy pressures will remain front and center, as higher prices at the pump often force consumers to cut back elsewhere—a troubling dynamic amid a softening labor market and growing concerns about economic slowing.

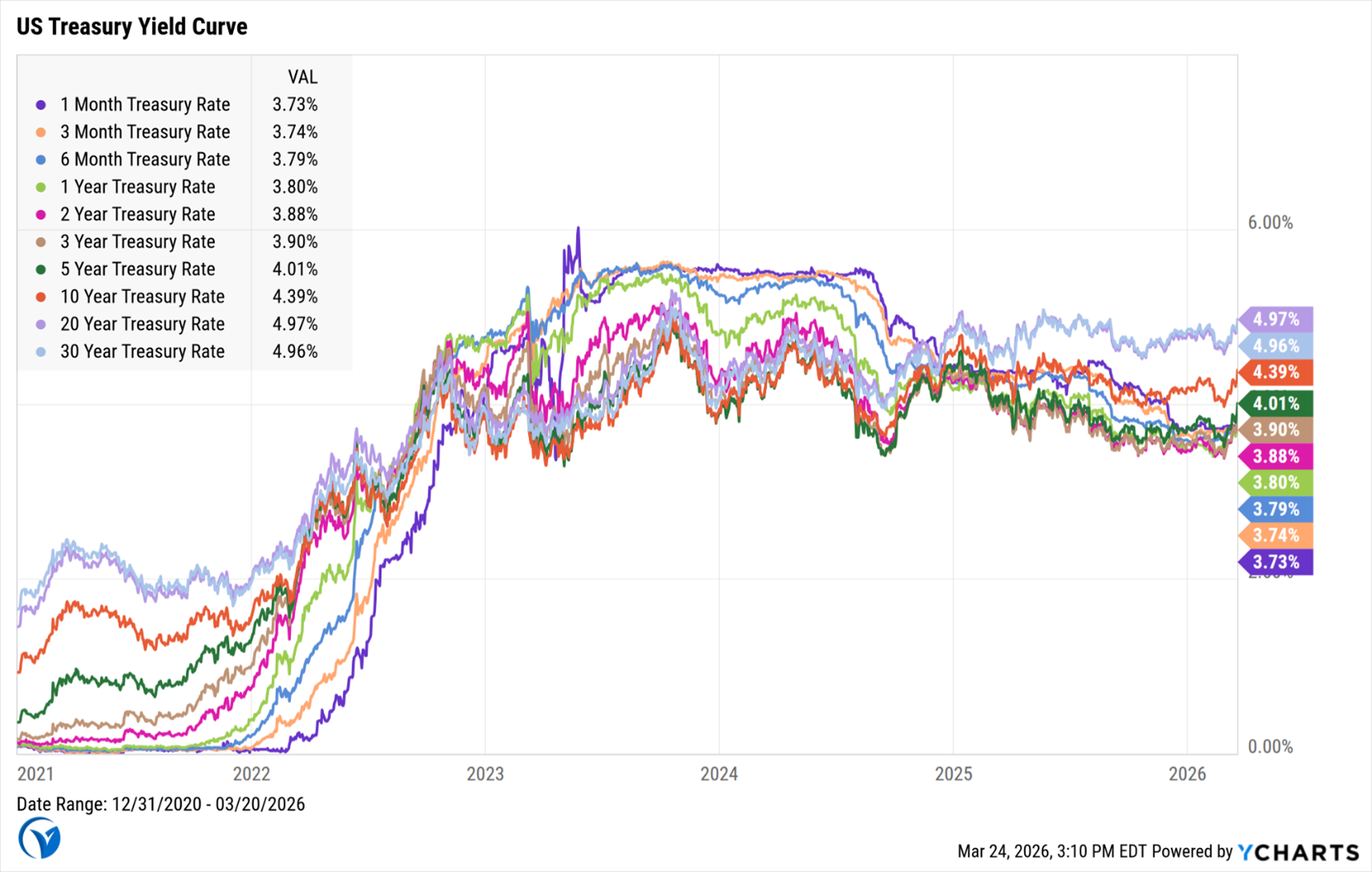

Bond and Equity Markets: Pricing Stagflation Risk

Amid the Iran conflict, fears of stagflation (slowing growth paired with rising prices) drove a sharp sell-off in equities and bonds throughout March. A Bloomberg index showed the Iran conflict erased from the value of global bonds, the biggest monthly loss in more than three years. Meanwhile, global equities shed approximately $11.5 trillion in market capital as investors rotated out of risk assets and repriced earnings expectations.

Typically, after a major geopolitical shock, volatility rises and risky assets such as equities and corporate bonds weaken, while U.S. Treasuries rally as investors seek safety. This time, however, Treasuries are not behaving like traditional havens. Instead, 10-year yields rose sharply following the attacks on Iran, driven by rising inflation expectations and diminishing odds of near-term rate cuts.

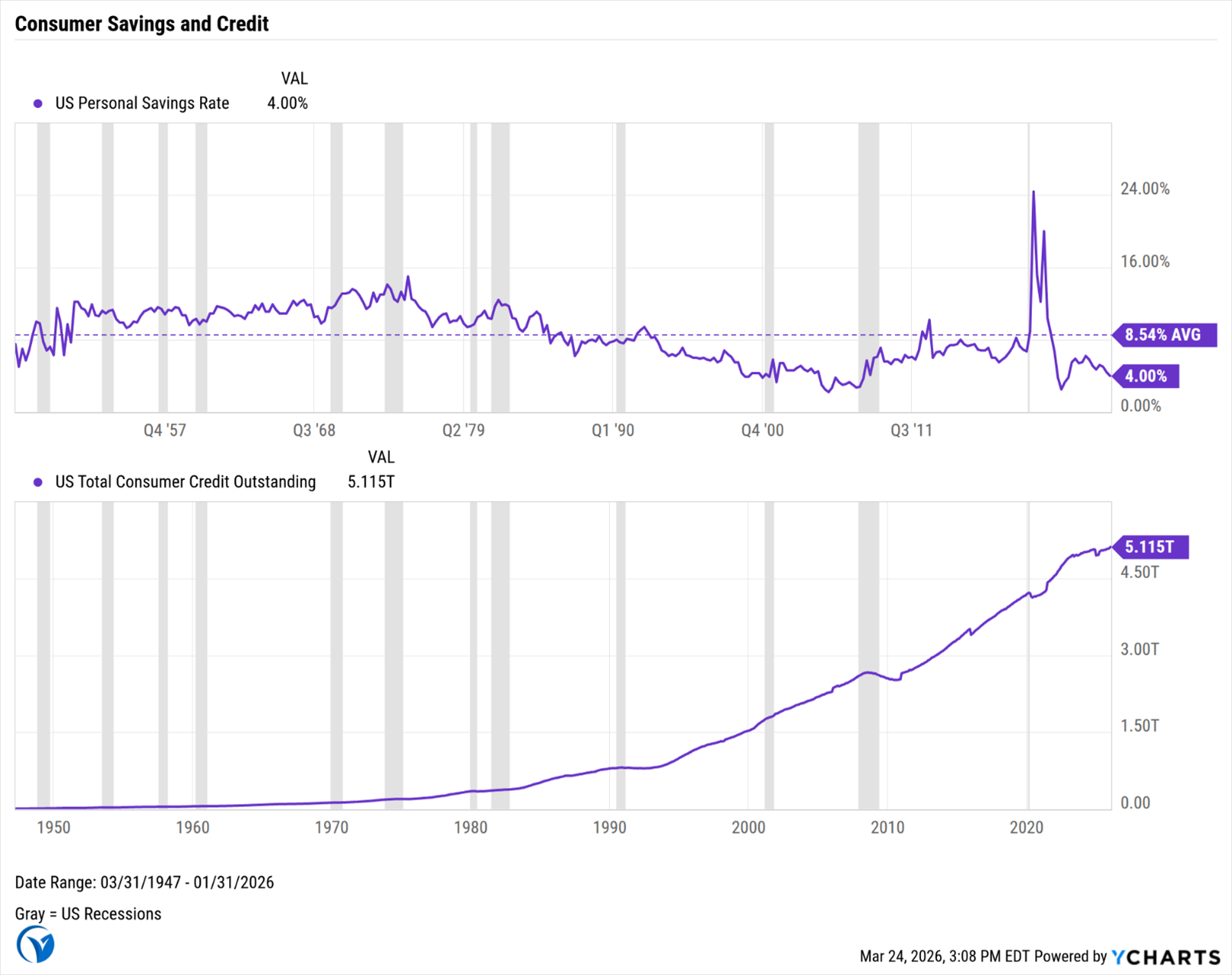

Consumer Credit: Delinquencies Continue to Rise

The Federal Reserve Bank of New York’s February report showed delinquencies rising to 4.8% of all outstanding household debt in Q4 2025, the highest since 2017. With rising defaults among younger and lower income borrowers listed as key drivers.

March data reinforced the view that household balance sheets are weakening at the margin, particularly for low income and younger borrowers. With the potential for inflation to reaccelerate due to energy shocks, this trend may worsen in the coming months.

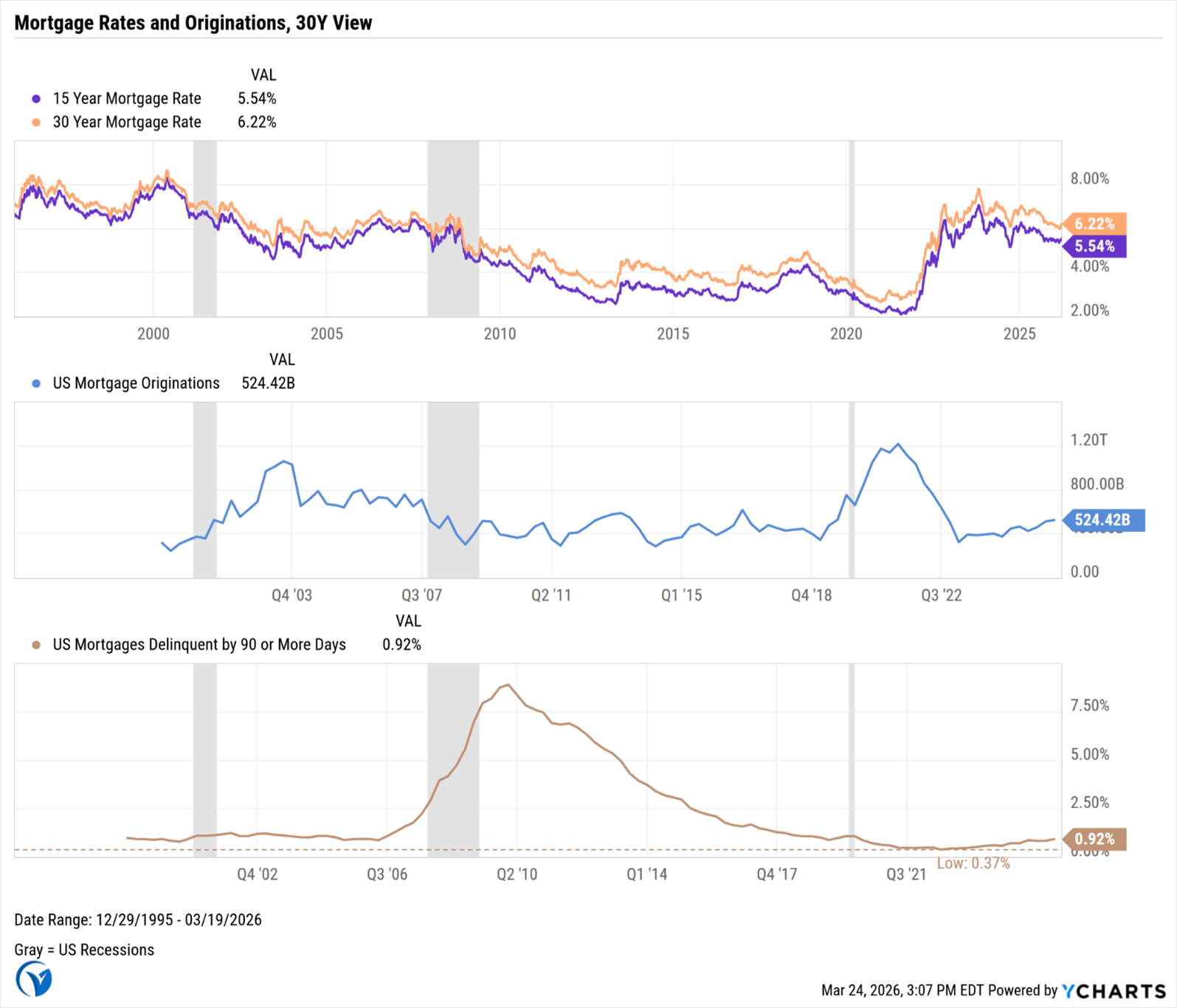

Housing and Mortgage Markets: Higher Rates Continue to Hit Demand

The housing sector faced renewed pressure in March as mortgage rates climbed along side bond yields. The average 30-year fixed mortgage rate rose to 6.22% on March 19, up from 6% at the start of the conflict, according to Freddie Mac.

Building products manufacturers have been hit particularly hard. Persistent inflation, elevated living costs, and higher mortgage rates have weighed on renovation spending and home buying throughout 2024 and 2025. Many large manufacturers reported Q4 earnings misses, and the Iran conflict now threatens to push mortgage rates even higher—potentially dampening the critical spring home buying season. These concerns have pressured the bond prices of building products manufacturers and related firms.

However, Fannie Mae and Freddie Mac stepped in with significant purchases of mortgage-backed securities, aiming to take advantage of wider spreads created by the selloff. Their intervention may help cushion the impact of the conflict on mortgage yields.

Federal Reserve Outlook

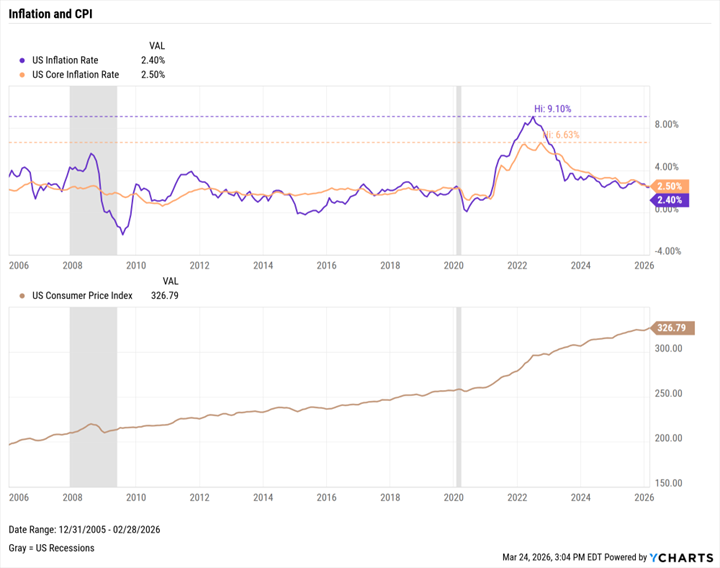

The Fed held rates steady at its March 17-18 meeting, but the path forward has become more uncertain. Oil and gas remain crucial across electrical generation, transportation, and feedstocks for petrochemicals like plastics in consumer goods. Lower supplies can drive inflation by directly increasing energy bill sand gasoline costs, and indirectly by raising shipping and production costs which businesses often pass onto consumers. Accordingly, the probability of a rate cut has decreased, and the possibility of a rate hike at the Fed’s April 28-29 meeting is not off the table.

Conclusion

March reiterated how quickly the market narrative can shift when geopolitical risk mixes with structural concerns. Private credit faced its most significant stress test in over a decade, energy markets absorbed a major supply shock, and both bonds and equities were repriced sharply as stagflation fears resurfaced. With delinquencies rising and mortgage rates climbing, the consumer and housing sectors are showing early signs of strain.

To summarize, we are navigating a Federal Reserve weighing inflation risks against slowing growth, a private credit market grappling with liquidity mismatches, and a geopolitical backdrop that remains highly unstable. In such an environment, flow of capital has historically favored a move toward defensive sectors, short duration fixed income, and inflation protected assets. Given the rapidly evolving nature of the current economy and geopolitical scenario, outcomes may shift if inflation cools faster than expected, if geopolitical tensions de-escalate and/or growth proves more resilient.

Disclosure: This piece is not intended as investment advice and has not been tailored to any specific individual's situation. It is for informational purposes only.