June 2025 Market Commentary

The first half of 2025 has been set against a backdrop of shifting macroeconomic conditions, the early impact of the Trump administration, and heightened geopolitical tensions. Investors are navigating a landscape of both risk and opportunity as they continue to deal with trends in the integration of private and public markets, evolution of digital assets, the fallout of a recent Treasury rating downgrade, and persistent inflationary pressures.

The Vera Planning Mid-Year Market Commentary highlights key developments across these areas and explains how we’ve incorporated these insights into thematic portfolios, aiming to capitalize on sector-specific trends.

Table of Contents

- The Macro-Economic Outlook

- Geopolitics and Impact on Commodity Prices and Rising Market Volatility

- Market Outlook and Sector Divergence

- Evolving Asset Management Industry Creates New Opportunities for Investors

- Crypto Market Dynamics

- What Vera has to Offer to Overcome the Evolving Markets

Vera Planning

Investment Committee and

Private Wealth Group

The Macro-Economic Outlook

The return of the Trump administration has brought renewed focus to protectionist trade policies, namely a sweeping set of tariffs that has disrupted global supply chains and threatened to raise input costs across several industries. While some tariffs have been temporarily paused, some—especially those targeting China—remain in place, contributing to inflationary pressures and overall, dampening consumer sentiment.

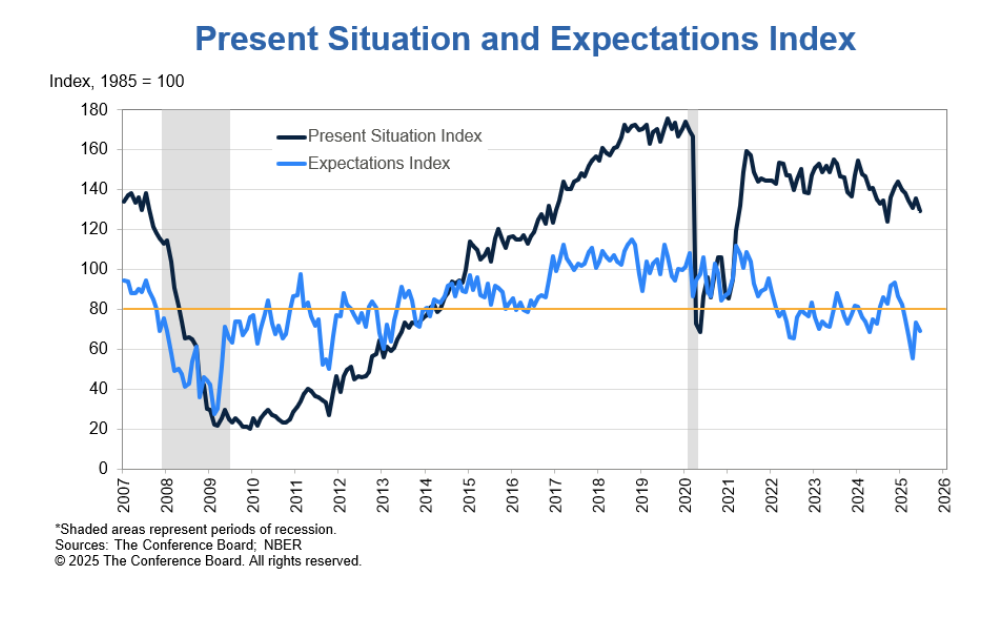

The Conference Board Consumer Confidence Index demonstrated a significant downtrend in June, declining by 5.4 points to 93.0 following a period of modest gains in May. This broad-based contraction was evident across its constituent components: the Present Situation Index decreased by 6.4 points to 129.1, and the Expectations Index fell 4.6 points to 69.0. The latter figure is particularly noteworthy, registering substantially below the 80-point threshold historically associated with an impending recession.

The sustained decline in the Expectations Index to this level warrants considerable attention, as its consistent performance as a forward-looking indicator has provided early signals for past economic downturns, suggesting that consumers are increasingly anticipating a less favorable economic environment over the near term.

Meanwhile, the stop-start approach—marked by the rapid imposition, selective suspension, and inconsistent enforcement of tariffs—has fueled significant uncertainty across global supply chains and corporate planning, while also unsettling financial markets.

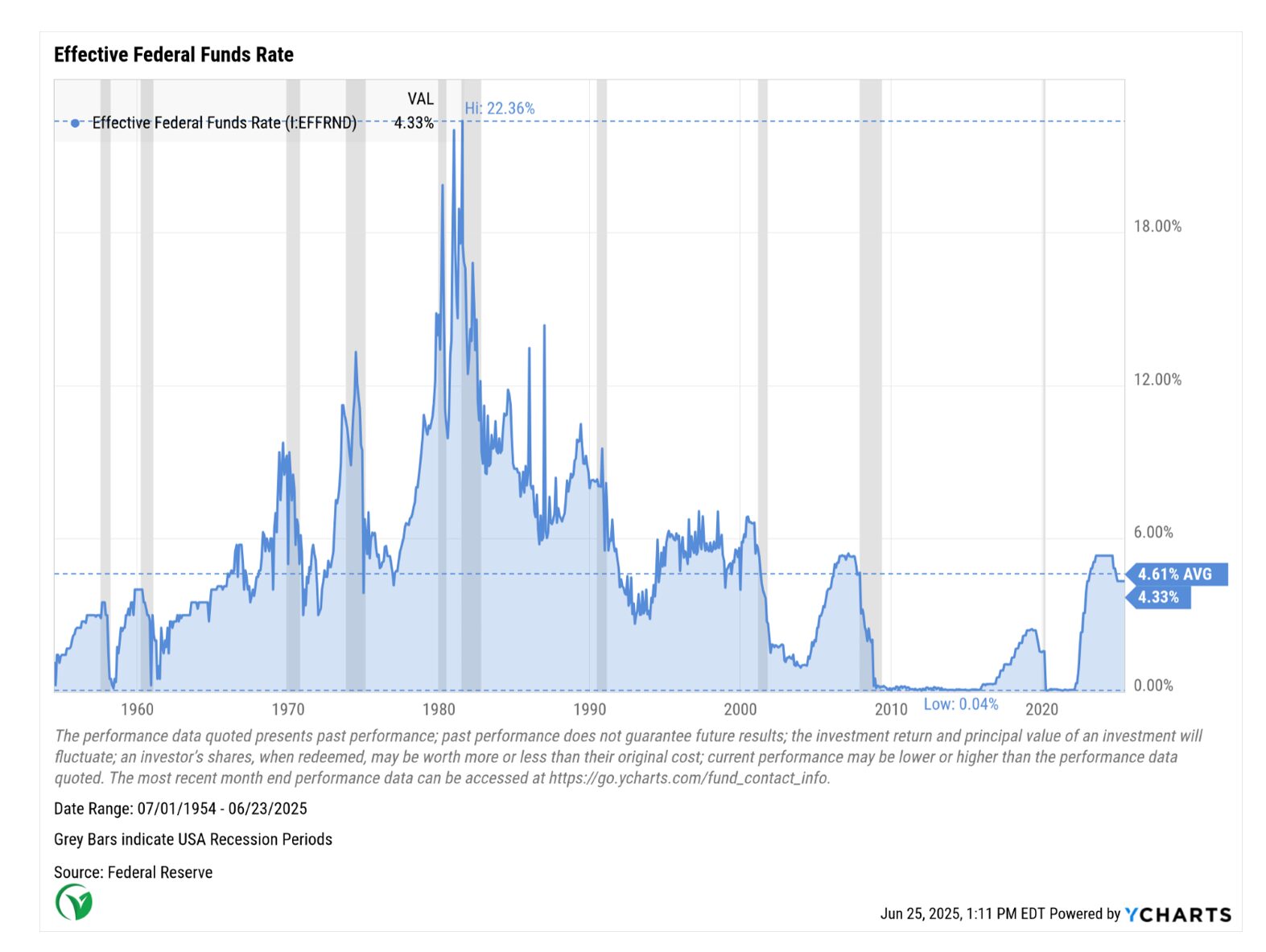

Trade-related uncertainties are compounded by growing concerns about the broader fiscal landscape, underscored by Moody’s recent downgrade of U.S. sovereign debt. On May 16, the credit rating agency lowered the U.S. rating from AAA to AA1, citing rising national debt and persistent fiscal deficits projected to grow from 6.4% of GDP in 2024 to nearly 9% by 2035. This marks the first time all three major credit rating agencies have rated U.S. debt below AAA status. In this environment, running sustained deficits has become increasingly difficult, as elevated interest rates significantly raise the cost of government borrowing. The Federal Reserve, wary of reigniting inflation amid ongoing tariff pressures and geopolitical uncertainty, has maintained a cautious ‘wait and see’ approach—holding the Fed Funds rate steady at a 4.0–4.25% target since December 2024. A modest uptick in inflation—rising 0.1% in May—has pushed the annual rate to 2.4%, further clouding the outlook for monetary policy.

Complicating the picture are regulatory developments in AI, Cryptocurrency, and tax reform. President Trump’s One Big Beautiful Bill Act proposes tax cuts, an increase in funding to border security and defense initiatives, and cuts in funding to programs like Medicaid—measures that are expected to add approximately $3 trillion to the national debt over the coming decade. At the same time, the bill also seeks to block state-level AI regulation for 10 years, a move that has drawn criticism from advocates and state lawmakers who argue it undermines local efforts to address algorithmic harms and consumer safety. In the cryptocurrency space, the administration has signaled support for a national regulatory framework in collaboration with the SEC.

A key development is the Senate’s recent passage of the GENIUS Act, which would establish federal oversight and regulations for stablecoins, a type of cryptocurrency often pegged to a currency like the U.S. dollar—now pending review in the House. Although the bill includes conflict-of-interest provisions for members of Congress, it notably exempts the president and their family, drawing criticism amid reports that President Trump has profited from the issuance of stablecoin USD1 by World Liberty Financial, a firm closely tied to his business interests. These moves reflect broader policy shifts favoring growth and deregulation; even as questions about long-term fiscal sustainability and adequate consumer protection in these rapidly evolving spaces become more prominent.

Geopolitics and impact on commodity prices and rising market volatility

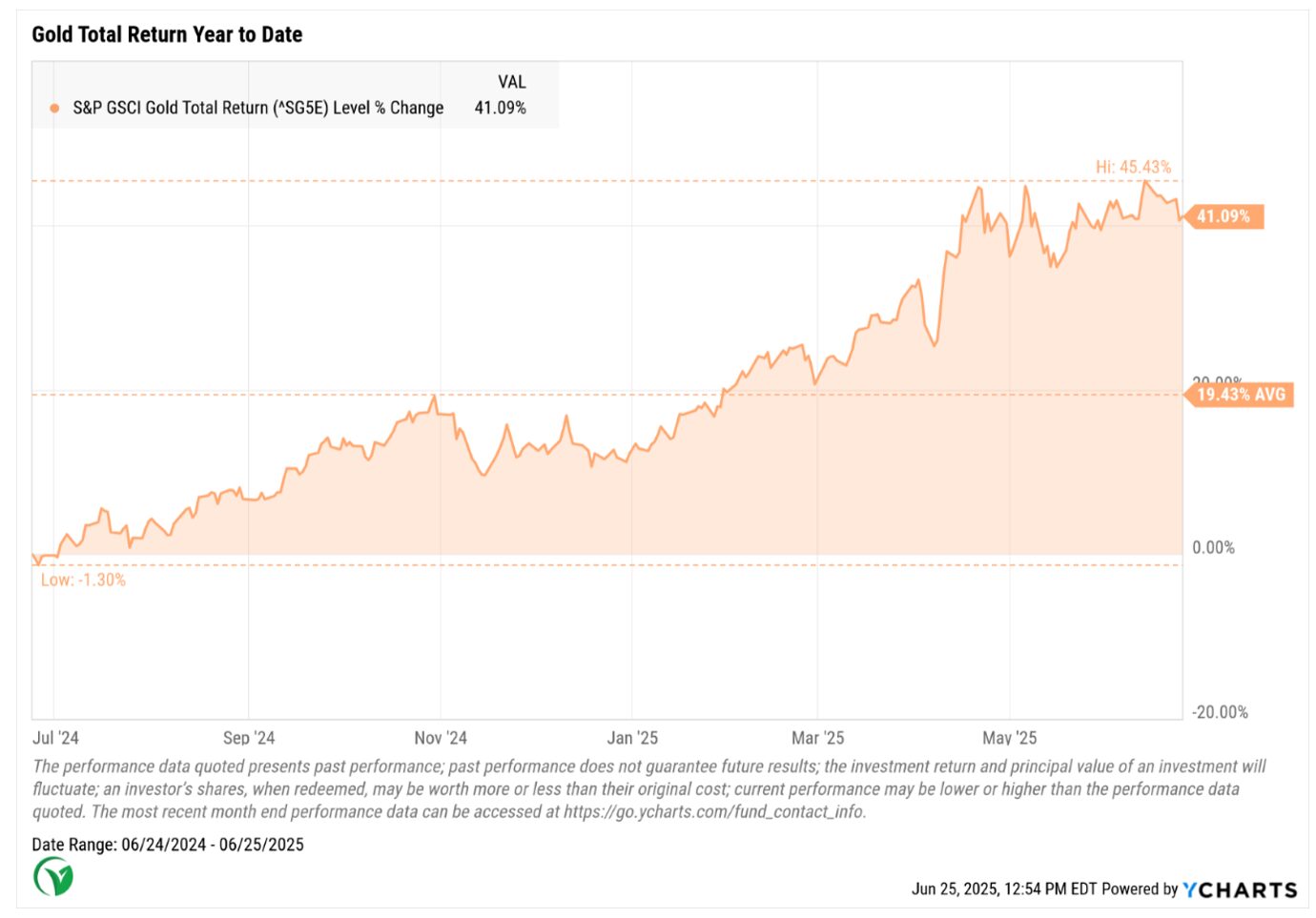

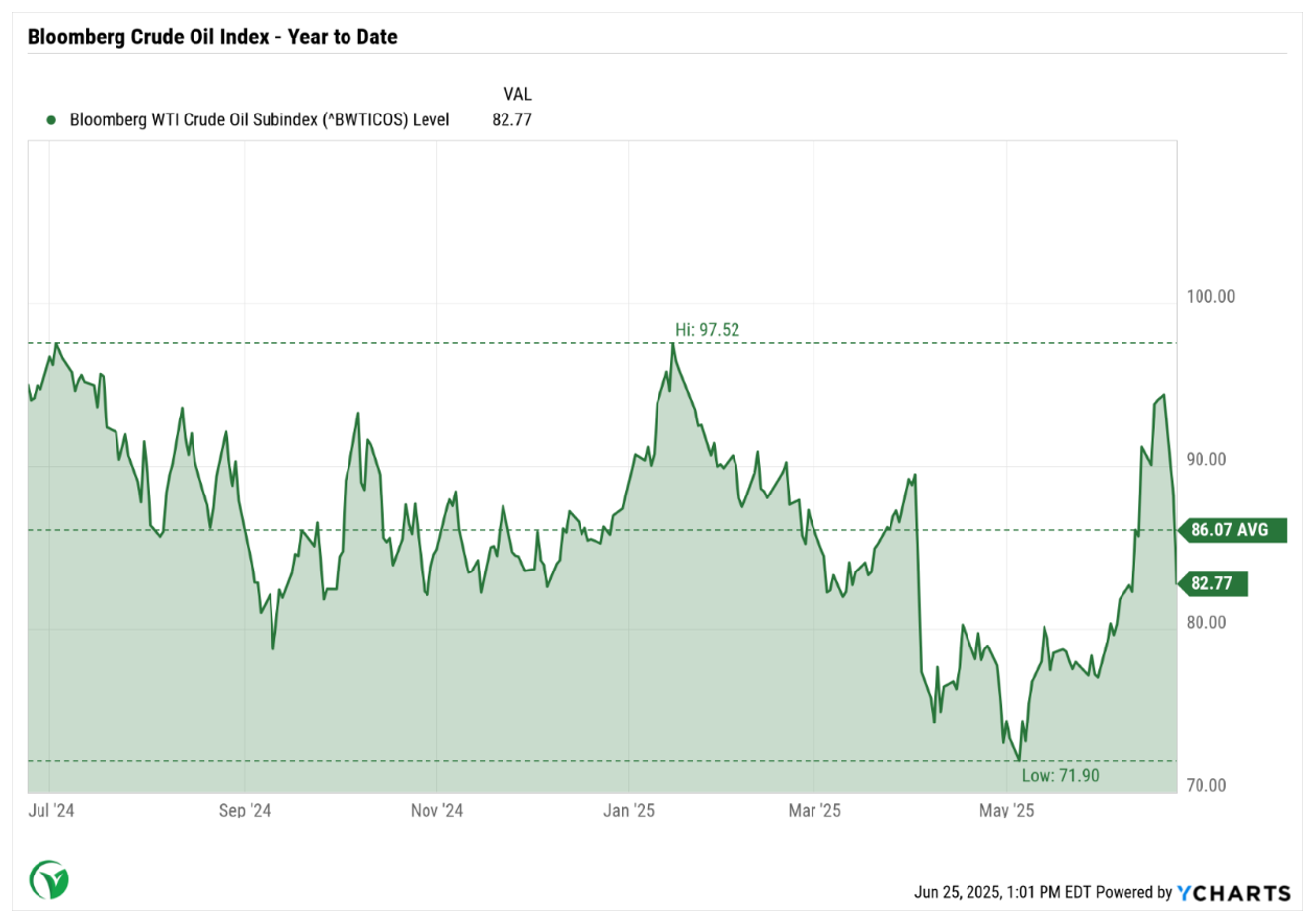

Geopolitical tensions have re-emerged as a dominant force shaping commodity markets and investor sentiment in 2025. The Iran–Israel conflict, which escalated in mid-June, triggered sharp movements in global commodity prices. Strikes on Iran’s South Pars gas field pushed WTI crude up 7% to $73 and Brent to $78.50, while the strategic risk around the Strait of Hormuz added a geopolitical premium to oil benchmarks. Safe-haven assets also surged—gold rose 45% to $3,446 and silver hit a 13-year high. Equity markets responded with a sectoral divergence: oil refining and mining companies rallied strongly in the days following the escalation, while gold miners outperformed on the back of rising bullion prices. Broader indices, however, showed mixed reactions—initial declines were followed by a rebound, with the Dow, S&P 500, and Nasdaq all closing higher on June 17 as markets digested the conflict’s implications

Beyond the Middle East, the Russia–Ukraine standoff continues to strain European energy and food supply chains.

Simultaneously, tensions between India–Pakistan and Israel–Palestine and Isreal-Iran are contributing to broader regional instability. Though varied in scope, these conflicts share a common outcome: heightened volatility and asset repricing. The VIX index spiked to 22 in June, marking a shift in the volatility regime. Defensive sectors like energy, financials, and aerospace have outperformed, while cyclicals and emerging markets remain vulnerable to geopolitical and policy shocks.

Trade policy has also returned to the spotlight. The U.S. administration’s renewed tariff strategy—ranging from 10% to 50%—is reshaping global supply chains and prompting retaliatory measures. These shifts are particularly disruptive for globally integrated sectors like technology and autos, fueling inflationary pressures in the U.S. while slowing growth in export-heavy economies. Equity markets have become more reactive to geopolitical headlines, with increased intraday swings and a rotation toward defensive and inflation-sensitive assets. These dynamics underscore the importance of tactical positioning, sectoral diversification, and adaptive portfolio construction in navigating today’s complex global landscape.

Market Outlook & Sector Divergence: Fed Policy, Defense Outperformance & Gold Rally

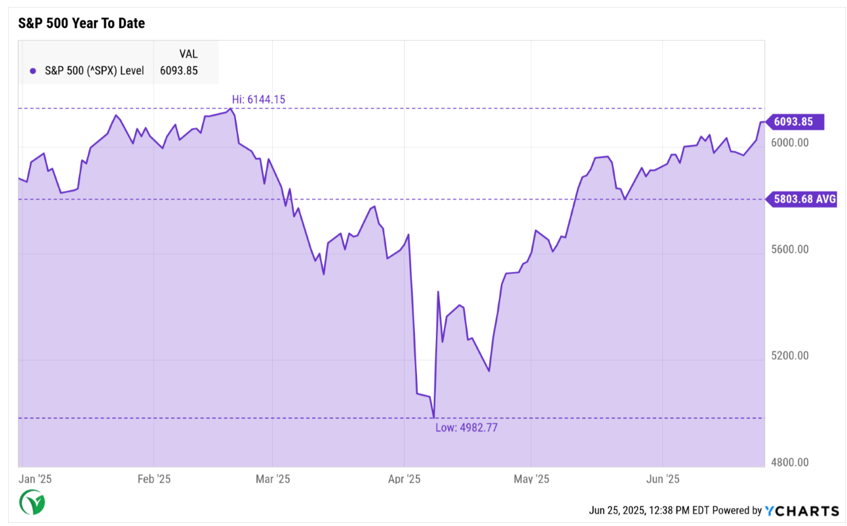

As of June 23, 2025, the U.S. equity market remains narrowly led by large-caps: the S&P 500 sits at 6,025.17 (+2.4% YTD) while the Russell 2000 lags at 2,132.68 (–4.4% YTD). At its June meeting, the Fed held rates at 4.25–4.50% and its dot plot still implies two 25 bp cuts by year-end, though a growing cohort of policymakers now argues for no cuts in 2025 amid sticky inflation and uneven growth. That split in view, combined with mixed economic indicators, has kept broad market gains modest.

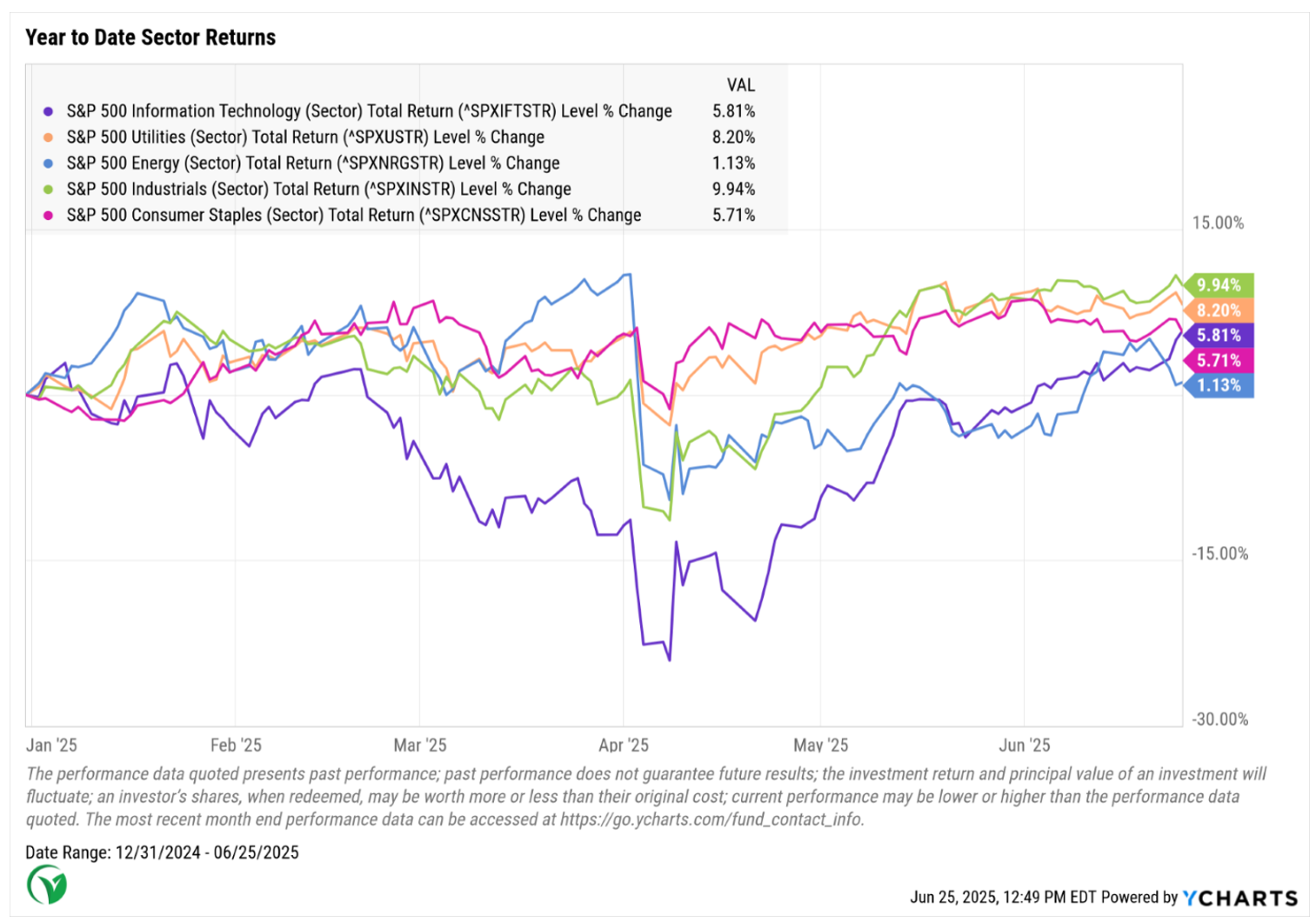

Sector returns have been highly dispersed. Aerospace & Defense stocks have surged ahead—with the Industrials sectors up roughly +9.94% YTD—driven by elevated defense budgets and geopolitical concerns. Energy (O&G) has been steady, with +1.13% YTD as oil and gas prices normalized after 2024’s swings. Technology’s headline +3–6% gain belies the fact that only a handful of mega-cap AI and cloud leaders have carried the group, while semis stumbled on new export restrictions to China. Industrials and Financials posted healthy mid- to high-single-digit advances, whereas Consumer Staples is flat to ~6% on consumer pressure. Defensive sectors—Utilities and Staples—have delivered low-to-mid single-digit returns, buoyed by reliable dividends.

Gold’s rally has underscored market caution: bullion is up about +15% YTD, trading near a record $3,360/oz, as investors seek refuge from inflationary and trade-policy uncertainties. Gold miners and broader commodities have likewise benefited, reinforcing gold’s role as a portfolio hedge when equity leadership narrows.

Evolving Asset Management Industry Creates New Opportunities for Investors

BlackRock CEO Larry Fink’s “50-30-20” vision—allocating 50% to public markets, 30% to private markets, and 20% to cash or short-term assets—has helped shape a broader movement in asset management. Firms like Vanguard, through its partnership with Wellington, are now offering blended investment products that combine public equities and bonds with private credit and infrastructure. This shift is designed to give individual investors access to more diversified portfolios and the potential for higher long-term returns, once only available to large institutions.

To support this evolution, the SEC has been easing access to private markets for individuals. While accredited investor rules still apply in many cases, new fund structures like interval and tender-offer funds, along with lower minimums (as low as $25,000), are making private market exposure more accessible. These vehicles offer a balance between access and oversight, allowing retail investors to participate in private assets while maintaining some liquidity and regulatory safeguards.

Looking ahead, investors can benefit from broader diversification and potentially enhanced returns, but they must also navigate challenges like limited liquidity and opaque pricing. To improve transparency, Moody’s is preparing to rate private credit markets, JPMorgan has launched a direct pricing team, and Aumni is helping standardize private asset valuations. These efforts aim to bring more clarity and confidence to private investing, helping investors make informed decisions in a space that’s rapidly becoming part of the mainstream portfolio mix.

Crypto Market Dynamics: DeFi Resurgence, Stablecoin Oversight, Memecoin Unwind & Mining Scale-Up

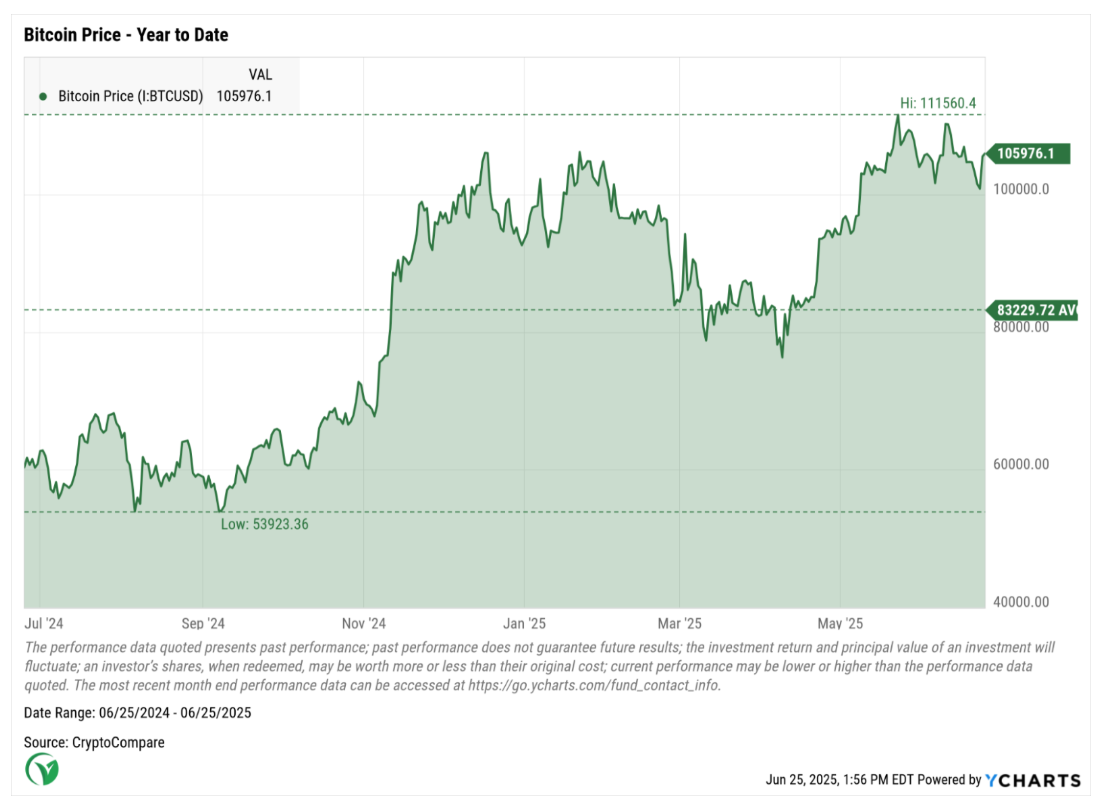

Bitcoin’s steady advance has been amplified by the proliferation of spot-Bitcoin funds, which are collectively up around +9–10% YTD, giving investors seamless BTC exposure through traditional brokerage platforms. Beyond Bitcoin, decentralized finance (DeFi) has roared back to life—Total Value Locked (TVL) in leading protocols has climbed roughly 40% since late 2024 to about $55–60 billion. Major lending platforms saw TVL surge 50–60% in just two months this spring, while emerging peer-to-peer engines grew deposits by nearly 40% as institutions sought yield-driven on-chain strategies—from over-collateralized borrowing to tokenized real-world assets.

On the stablecoin front, the June 17 passage of federal legislation now requires large issuers (>$10 billion outstanding) to hold 1:1 dollar reserves, submit monthly third-party audits, and enforce full AML/KYC standards—bringing top dollar-pegged tokens under uniform federal oversight. With overall stablecoin market capitalization having steadied in H1, this clear framework is expected to bolster confidence in on-chain payments, DeFi collateral pools, and institutional treasury operations.

By contrast, speculative memecoins have been crushed: top tokens are down 50–85% YTD as hype-driven pumps gave way to investor fatigue. While new meme-themed coins continue to launch, most have fared poorly, underscoring how crypto markets are maturing—shifting focus from frothy speculation toward projects with genuine utility.

Finally, Bitcoin mining infrastructure is undergoing its largest expansion ever. Publicly traded miners are racing to scale: the largest operators now each exceed 50 EH/s of hash rate, deploying tens of thousands of next-generation ASICs and securing direct power deals to minimize cost per coin. This arms race in energy-efficient, vertically integrated operations is positioning the biggest miners to dominate post-halving rewards and strengthening network security as Bitcoin heads toward its next supply reduction.

What Vera has to offer to overcome the evolving markets

In today’s dynamic market environment, Vera is advancing its commitment to client wealth creation by introducing a suite of investment solutions that combine diversification, customization, and strategic exposure. These offerings are designed to help clients navigate uncertainty while aligning portfolios with long-term goals.

At the foundation of our platform are Genesis and Prime, two multi-asset model portfolios built on robust quantitative screening and diversified across asset classes, geographies, and market caps. Genesis is ETF-centric, offering three risk-based models tailored for both tax-sensitive and non-tax-sensitive investors. It blends fixed income and equity ETFs to deliver balanced exposure aligned with clients’ investment policy statements. Prime, by contrast, provides a broader customization spectrum with five risk tiers and includes both direct stock selection and fixed income ETFs. It also offers 100% equity and 100% fixed income options, catering to clients with specific asset allocation preferences and a need for more granular control.

For clients seeking a more tailored and actively managed approach, Omega delivers personalized portfolios with continuous monitoring and rebalancing. This solution integrates individual investment goals, tax considerations, and constraints into a bespoke strategy. Omega is ideal for clients who value precision, adaptability, and a high-touch experience in their portfolio management.

Complementing these core strategies is our suite of Thematic Portfolios, which offer targeted exposure to transformative sectors and macro trends. Built around 12 distinct themes—such as Innovation, ESG, and Natural Resources—these portfolios are constructed using quantitative screening, with weights aligned to analyst conviction and optimization models. Thematics are ideal for investors looking to express a specific view or gain sectoral exposure. They can also be blended with other strategies, such as combining Aerospace Thematic with a Fixed Income Prime portfolio or integrating multiple themes into a single allocation. Regular rebalancing ensures profits are captured, and new opportunities are continuously explored.

Together, these offerings reflect Vera’s forward-thinking approach to portfolio construction. Whether through diversified multi-asset models, personalized mandates, or high-conviction thematic plays, Vera is moving decisively to support clients in building long-term wealth across market cycles. As we continue to evolve with the markets, our focus remains on delivering clarity, flexibility, and performance through every solution we bring forward.

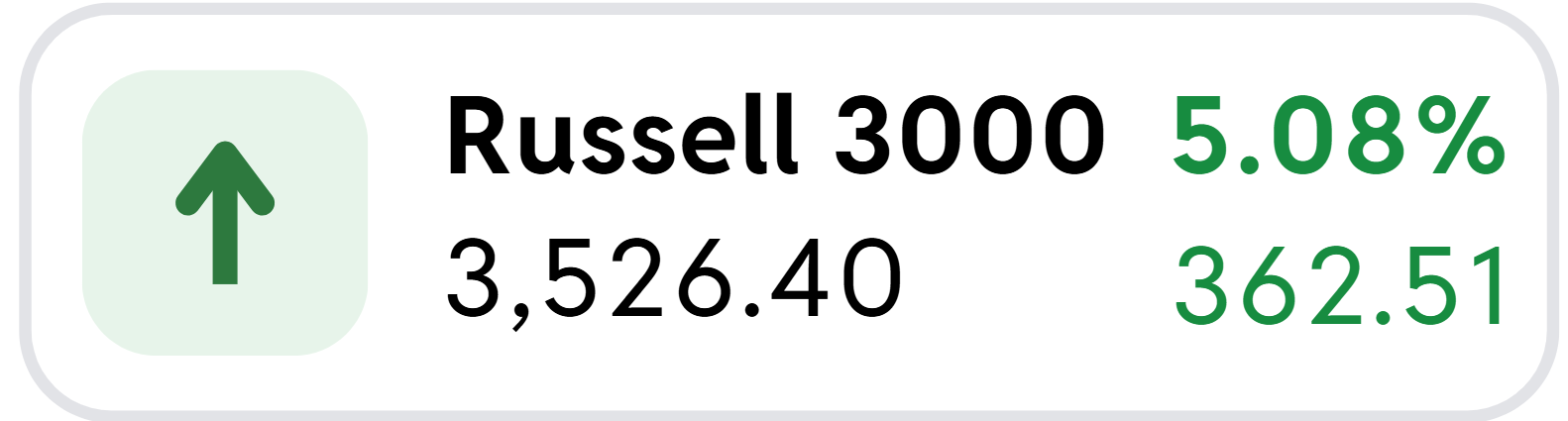

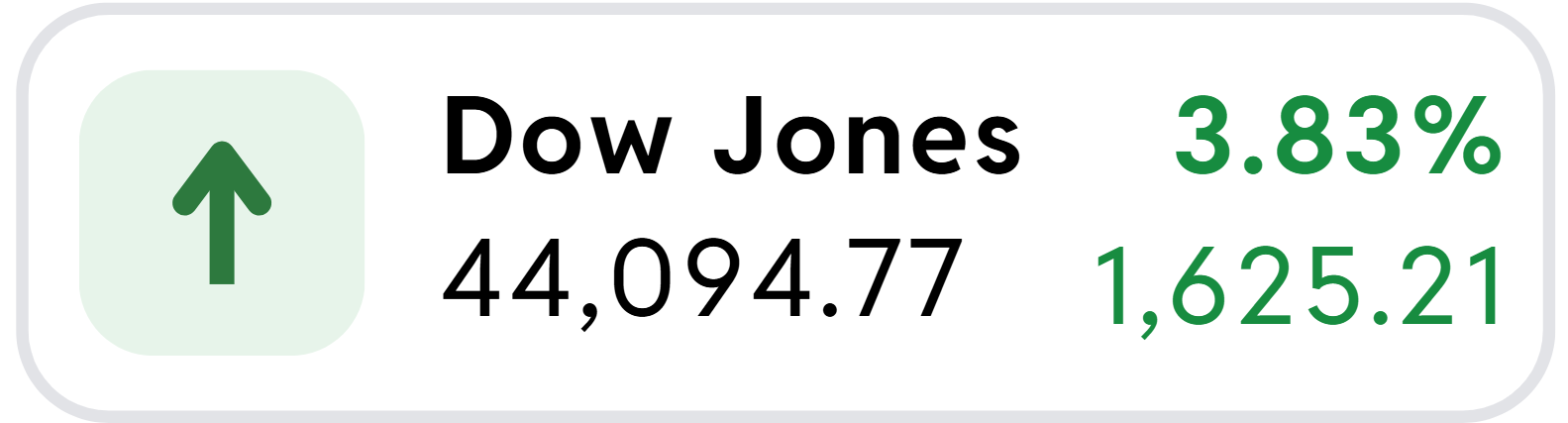

Key Market Indicies

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult a financial professional for your personal situation.

Past performance does not guarantee future results. Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Graphs provided by YCharts.

Key Market Indices according to Google Finance.

Securities offered through Registered Representatives of Cambridge Investment Research, Inc., a broker/dealer, member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. Cambridge and Vera Planning are not affiliated. The information in this email is confidential and is intended solely for the addressee. If you are not the intended addressee and have received this email in error, please reply to the sender to inform them of this fact. We cannot accept trade orders through email. Important letters, email, or fax messages should be confirmed by calling (678) 250-5099. This email service may not be monitored every day, or after normal business hours.