December 2025 Market Commentary

Market Lookback

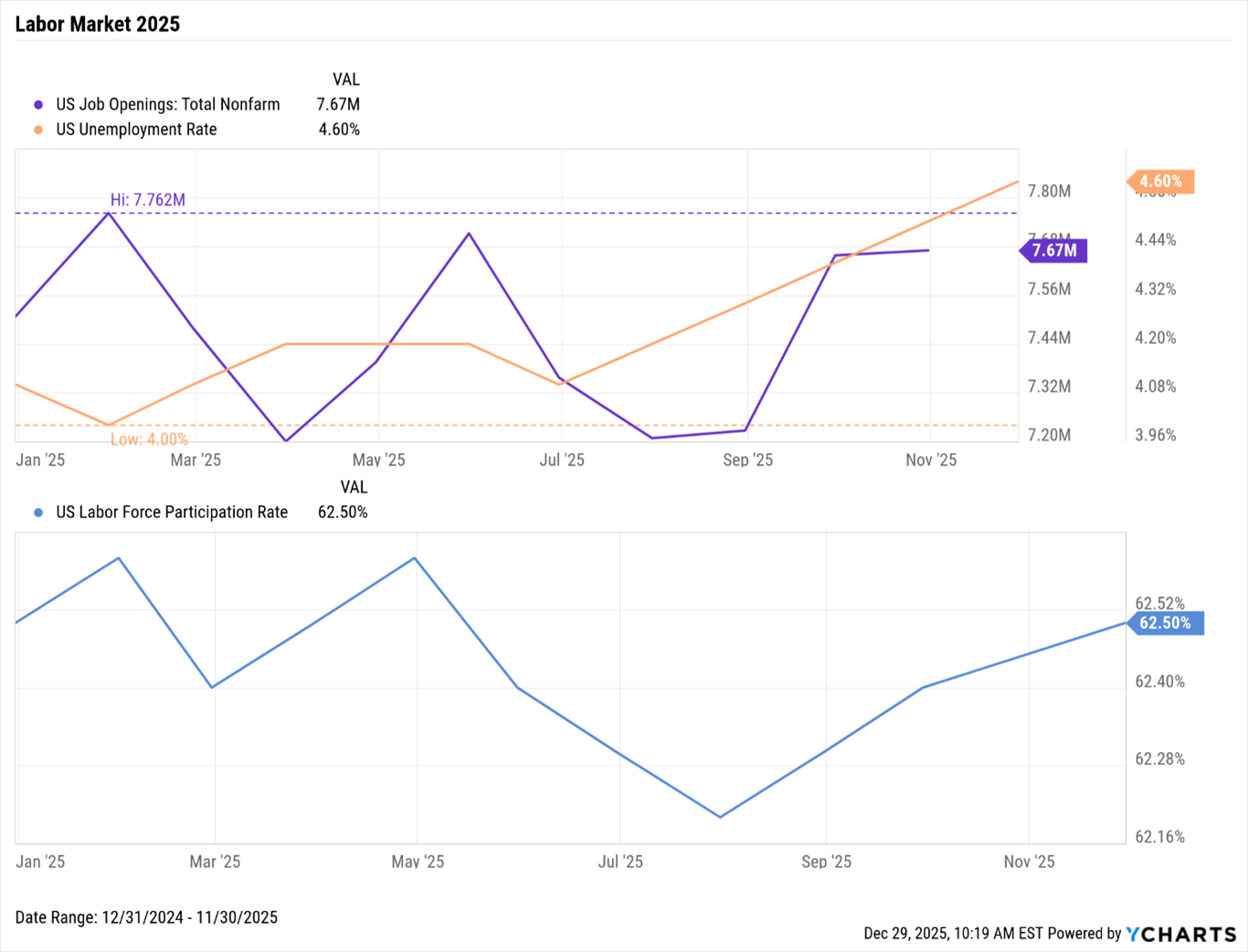

Macro Backdrop: Fed Policy, Inflation, Employment, and Rate Cuts

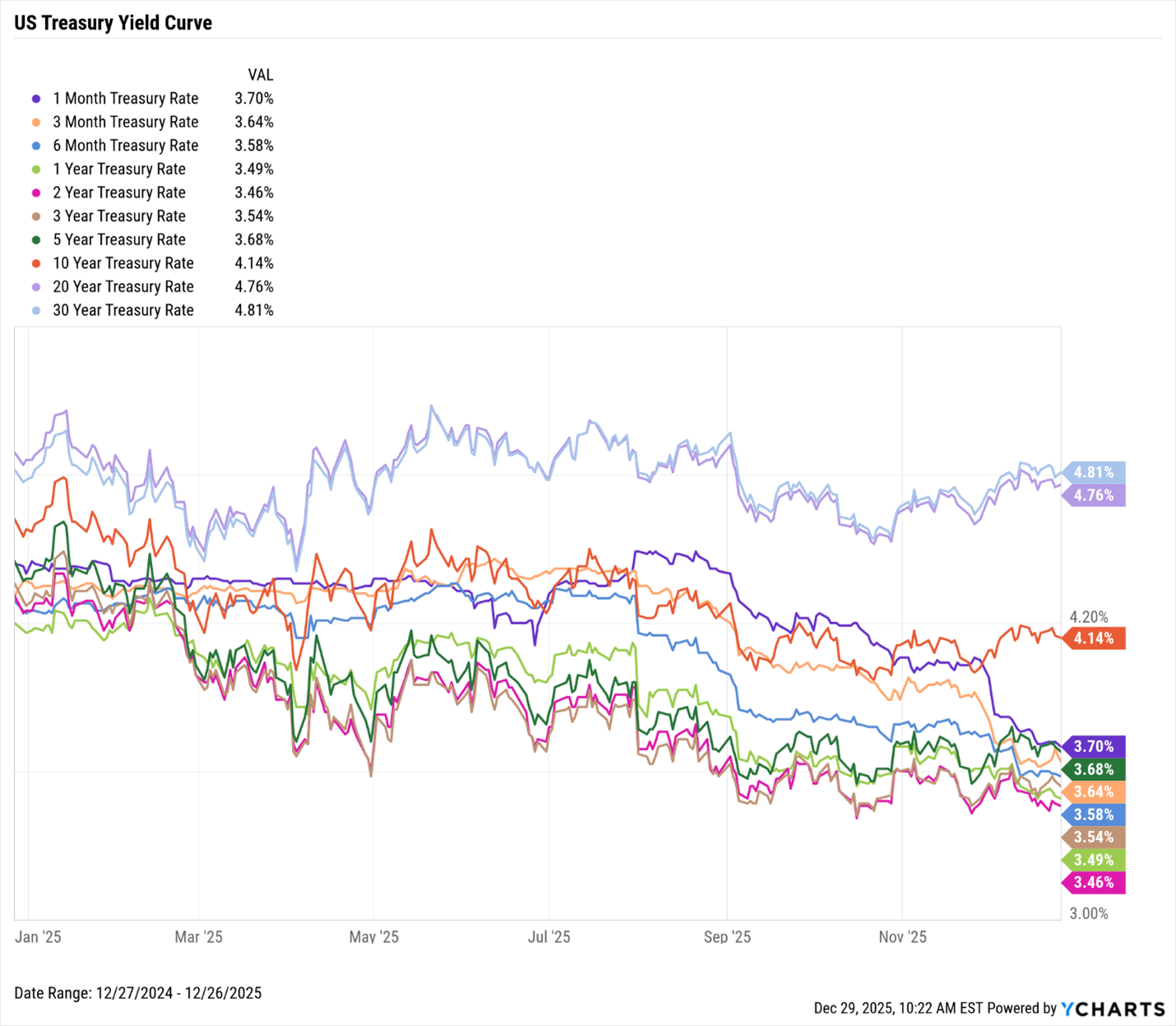

In 2025, the Federal Reserve played a pivotal role in shaping market sentiment and direction. For the first eight months of the year, the Federal Open Market Committee (FOMC) maintained a “wait-and-see” approach, keeping the federal funds target rate steady between 4.25% and 4.5%. However, emerging signs of weakness in the labor market prompted the Fed to take action, resulting in three rate cuts of 25 basis points each in September, October, and December. These reductions brought the target rate down to a range of 3.5% to 3.75% by year-end. The Fed’s moves were a direct response to shifting economic conditions and growing concerns over employment softness.

Key Macro Themes

Fed Policy Shift

Throughout 2025, the Federal Reserve navigated a complex policy environment. Inflation remained persistently above the central bank’s 2% target, while the labor market began showing signs of cooling. Policymakers entered the year with a restrictive stance, concerned that easing policy too soon could jeopardize progress on inflation. As job growth slowed and payroll reports continually missed expectations, discussions within the FOMC became increasingly divided. Dovish members emphasized the risks of keeping policy too tight and the potential harm to employment, while hawkish members warned against easing with inflation still elevated. This internal debate led to a cautious and contested shift toward rate reductions as the year drew to a close.

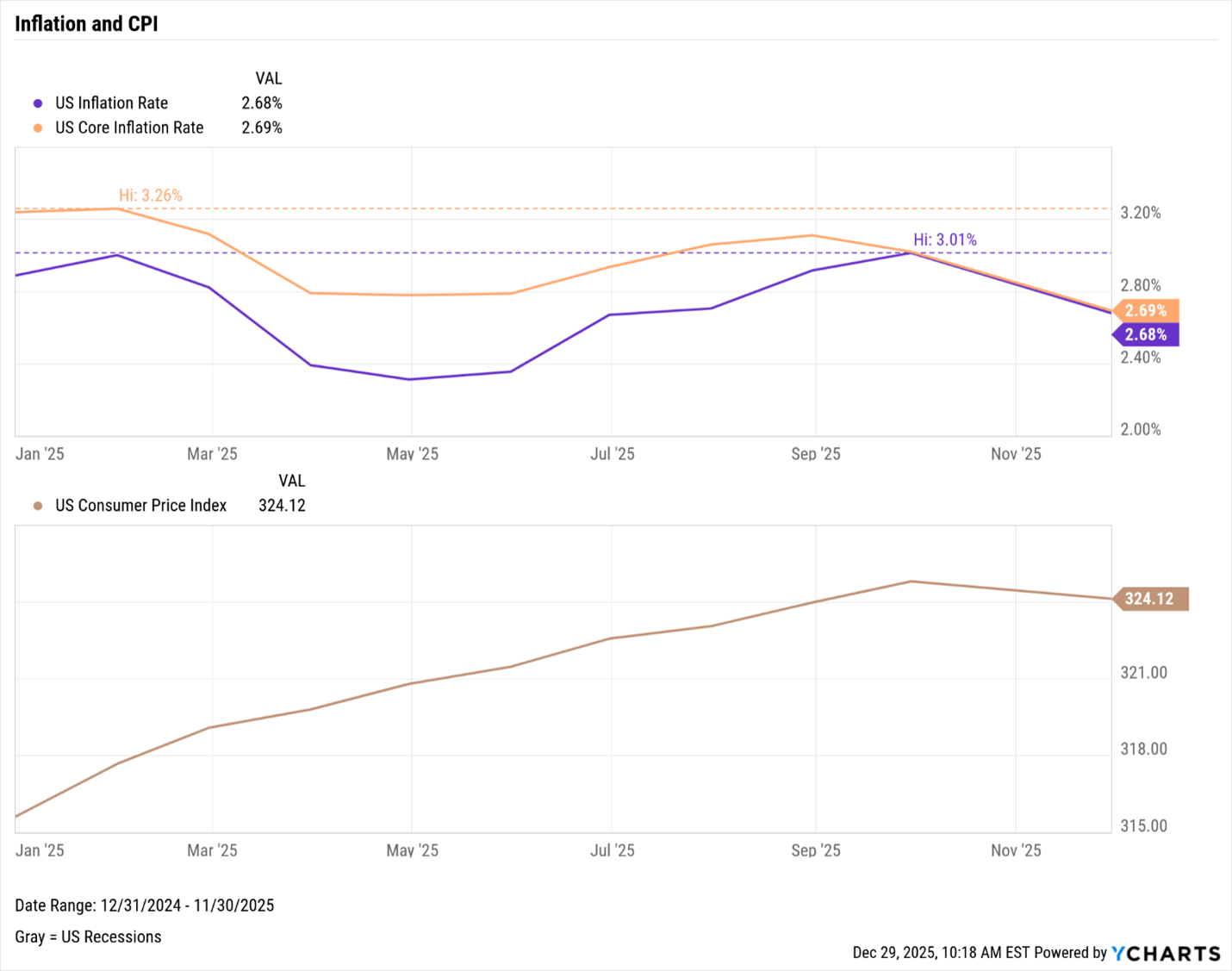

Inflation Trends

Inflation throughout 2025 persisted above the Fed’s 2% target, even as headline figures began to cool slightly. Consumers continued to face pressure from rising prices on essential goods such as bananas, ground beef, and coffee, which saw some of the steepest increases of the year. The Trump administration responded by implementing targeted tariff exemptions aimed at mitigating these price increases. The inflation picture was further complicated by a government shutdown in the fall, which disrupted the collection of Consumer Price Index (CPI) data. As a result, there was no CPI reading for October, and the November core CPI figure came in at 2.6%, heavily influenced by Black Friday discounts. Economists cautioned that this data likely understated the true level of inflation.

Rate Cuts and Market Impact

The Federal Reserve’s late-year rate cuts were met with a muted response from equity markets. Lower rates typically serve as a tailwind for equities, but the December cut failed to spark a sustained rally. Market participants remained cautious amidst ongoing macroeconomic uncertainty, concerns about the reliability of recent inflation data, and visible divisions within the FOMC regarding the future path of monetary easing.

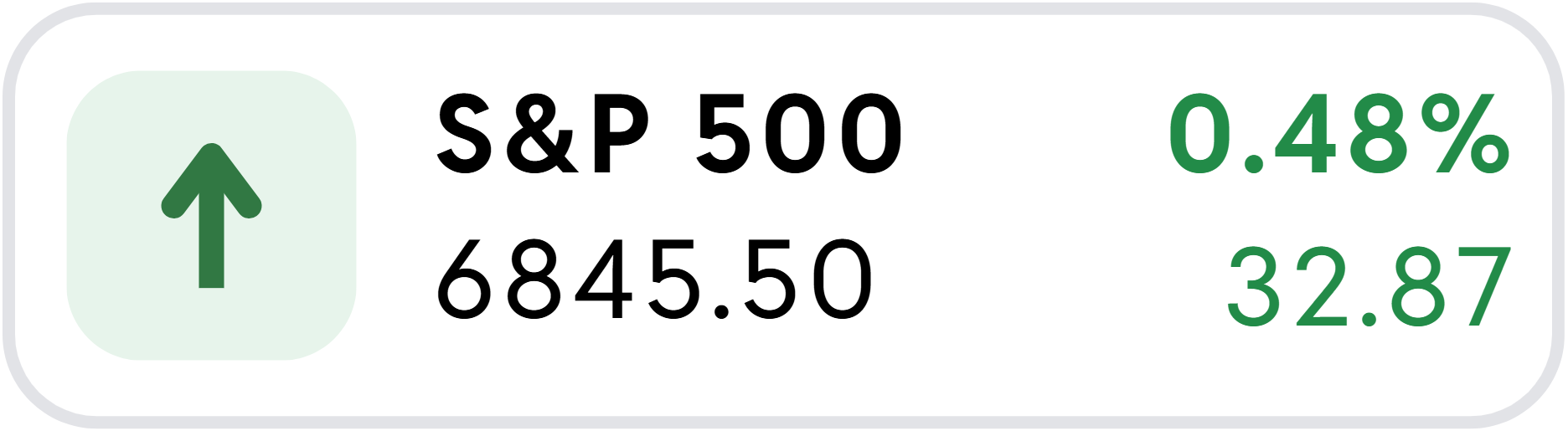

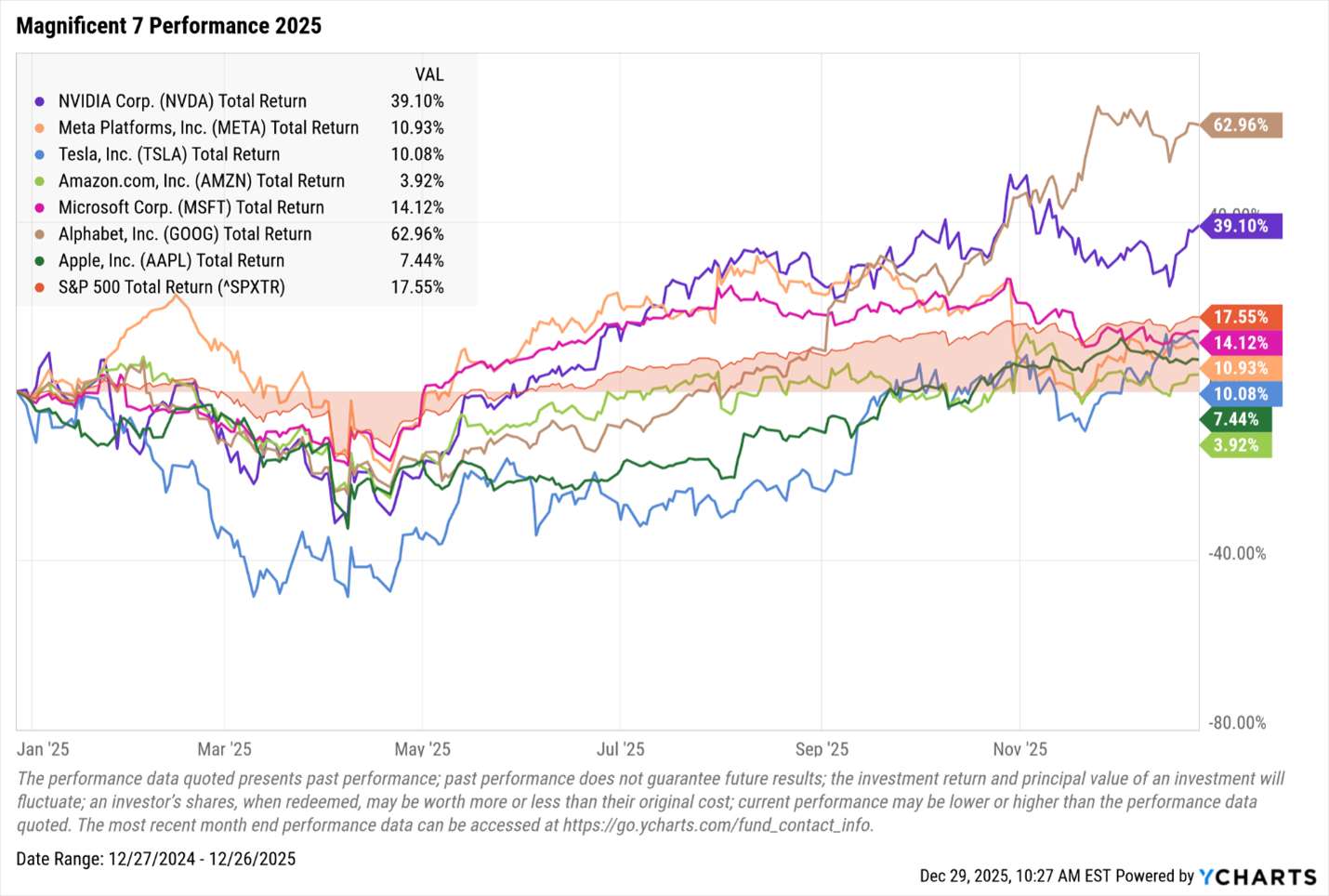

AI-Driven Equity Rally

Equity markets in 2025 were heavily influenced by continued expansion in artificial intelligence investment. Major indices, such as the S&P 500, saw gains largely driven by a select group of companies focused on AI infrastructure, advanced computing, and data-center development. As the year progressed, investor sentiment shifted from initial optimism to heightened caution, with closer scrutiny of AI-related valuations, spending, and prospects for monetization.

Overbuilding and Overspending Concerns

The rapid influx of capital into AI infrastructure raised concerns about possible overbuilding. Large cloud, hardware, and enterprise technology firms committed substantial resources to data-center expansion. By mid-2025, market participants began to question the sustainability of this spending, given limited near-term revenue opportunities. Companies deploying capital ahead of actual demand, expanding without clear monetization strategies, or relying on optimistic long-term AI revenue assumptions faced increasing valuation pressures. The market started differentiating between firms with established AI revenue streams and those with more aspirational positioning.

Circular Capital Flows Within the AI Ecosystem

A notable development was the rise of circular investment flows among major AI developers, cloud providers, and hardware manufacturers. These entities increasingly acted as customers, partners, and investors in each other’s businesses, creating a feedback loop that reinforced demand and capital deployment. By mid-year, skepticism emerged regarding whether this build-out was driven by genuine economic fundamentals or simply a closed loop of self-reinforcing investments.

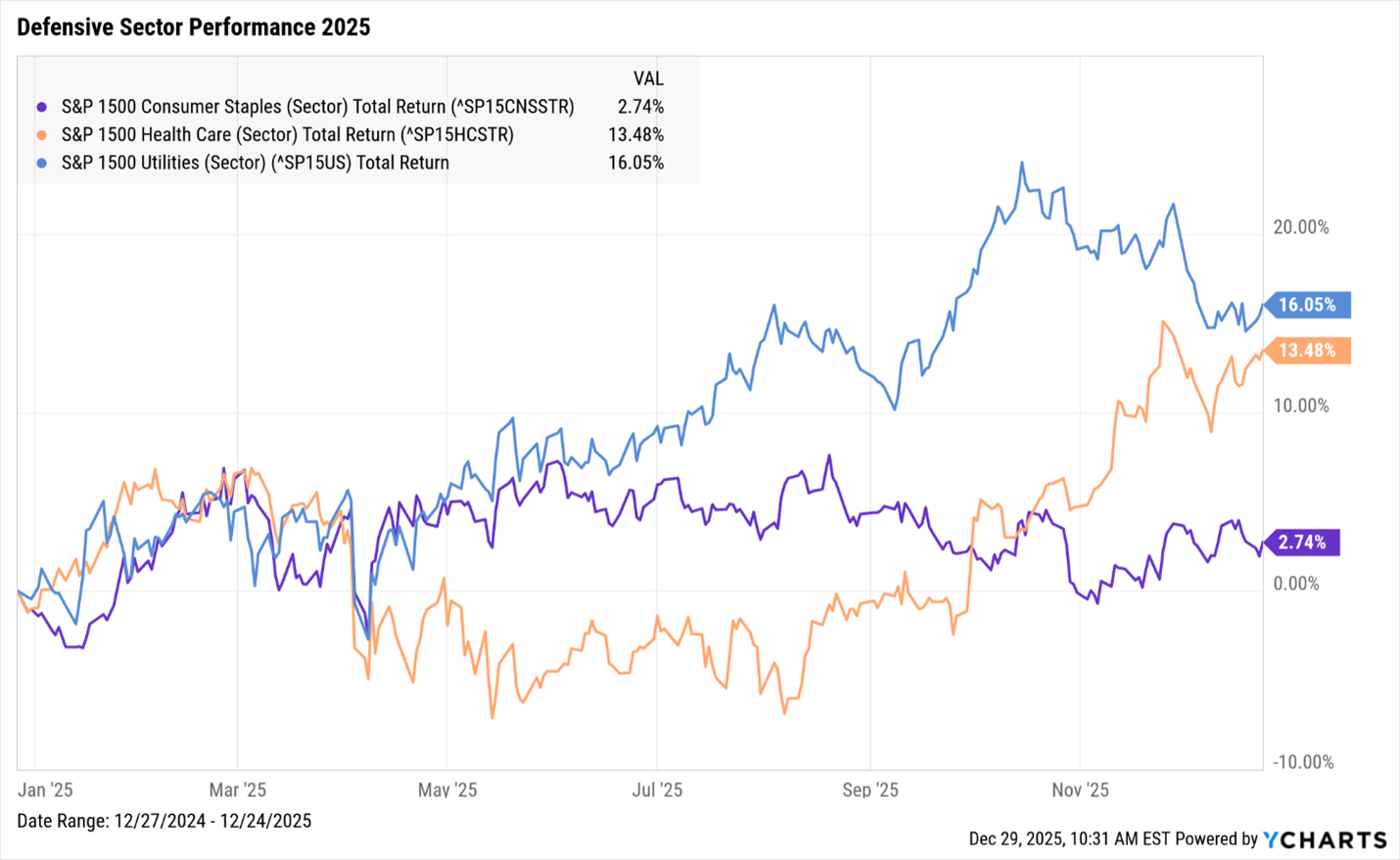

Rotation into Defensive Sectors and Flight to Safety

As concerns about stretched valuations in AI-focusedcompanies mounted, investors shifted to a more defensive posture. Capitalrotated into sectors with stable earnings, such as Healthcare and ConsumerStaples, especially toward the end of the year. Meanwhile, safe-haven assetsexperienced significant gains: Gold and Silver prices rose by over 64% and 120%, respectively, reflecting broad portfolio de-risking and skepticism aboutthe sustainability of the AI-driven rally.

Crypto Resurgence and Dip

Cryptocurrencies saw a major resurgence in 2025, fueled by improved liquidity, greater institutional involvement, and a more supportive regulatory environment. Following a subdued first quarter, digital assets accelerated in the summer and fall, with Bitcoin briefly surpassing $126,000. However, momentum faded toward year-end, and major cryptocurrencies—including Bitcoin—retreated from their highs, closing the year on a weaker note.

Institutional Adoption and ETF Inflows

Institutional participation in crypto markets expanded significantly throughout the year, largely driven by the rapid growth of spot-based Bitcoin ETFs. These products became some of the most actively traded instruments, attracting billions in net inflows. The increasing popularity of ETFs marked a shift in institutional access to digital assets, with regulatedstructures supplanting direct custody and bespoke trading arrangements, furthercementing crypto’s place in diversified portfolios.

Regulatory Tailwinds and Supportive Policy Environment

Regulatory advances played a crucial role for crypto in 2025. The GENIUS ACT established comprehensive standards for stablecoins,including guidelines for reserves, disclosures, redemption rights, andoversight. This clarity reduced counterparty risk, enhanced liquidity, and made stablecoins more attractive for institutional use in payments, collateral, andtreasury management. The Trump administration’s broadly accommodating stancetoward digital asset innovation, coupled with legislative clarity, bolsteredsector confidence and sustained inflows for much of the year.

Despite these supportive factors, the year ended with fadingbullish sentiment and profit-taking, resulting in a pullback in digital assetprices. This softness reflected broader market caution and mirrored trends another risk assets, underscoring the ongoing volatility and cyclical nature of the cryptocurrency market.

Conclusion

The year 2025 was marked by significant macroeconomic shifts, a contested monetary policy landscape, and evolving investment trends. From the AI-driven equity rally and its subsequent cautionary turn to the resurgence and mainstreaming of crypto assets, these developments underscore the importance of vigilance, diversification, and proactive risk management at Vera Planning. Navigating the complexities of modern markets requires ongoingattention to both macroeconomic signals and emerging investment themes.