April 2026 Market Commentary

April 2026 Market Commentary

Iran Conflict – Is the Cease-Fire Optimism Premature?

The Iran conflict has followed an erratic stop-start trajectory. A rapidly escalating conflict gave way to a two week cease-fire, which was set to expire April 23rd, but has since been extended with no specific end date. Meanwhile, the Trump administration has maintained aggressive posturing. Notably, President Trump stated shortly before the cease-fire that "a whole civilization will die tonight, never to be brought back again." Meanwhile, the U.S. Navy has imposed a blockade of Iranian ports and seized Iranian vessels during the cease fire.

The administration appears to be pursuing a strategy of sustained economic attrition, with the goal of pressuring Iran into larger concessions at the negotiating table. Whether that strategy succeeds is uncertain, but it does suggest the conflict timeline will be extended.

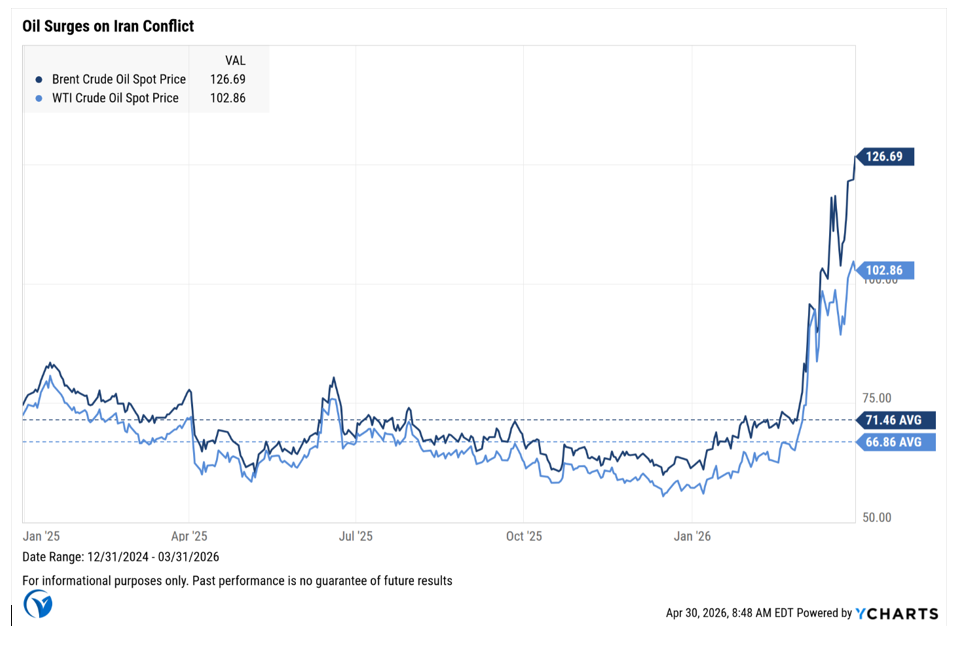

This marks bad news for the U.S. and global economies. Since the start of the conflict, Brent Crude surged past $100/bbl and has hovered at elevated levels since. The cease-fire briefly pulled prices toward $97-98 before they rebounded to approximately $105 on April 23, as optimism over the truce faded.

Equity Markets & Potential for Correction

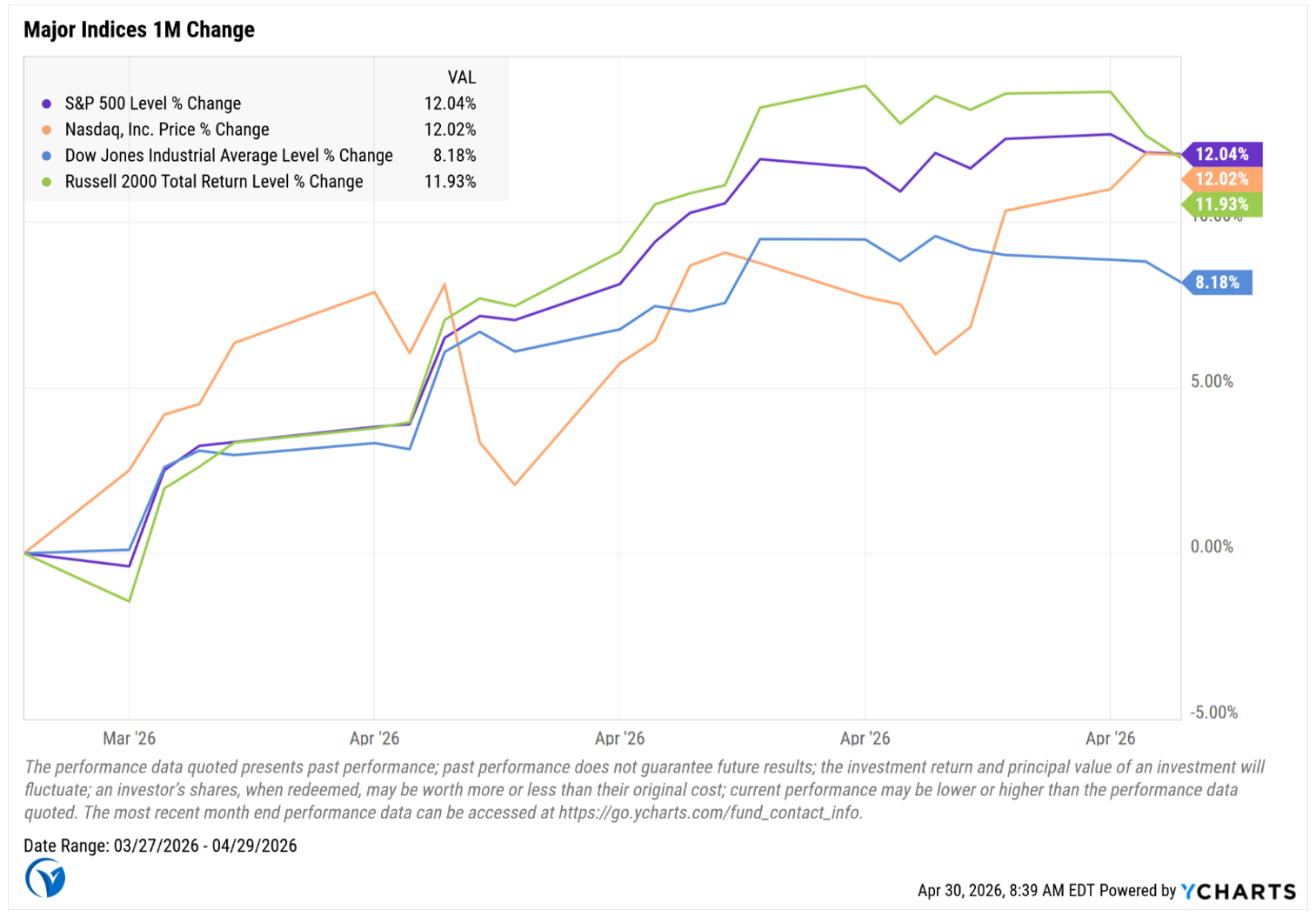

Equity markets rallied sharply on the cease-fire, effectively erasing conflict-driven losses. In fact, the S&P 500 achieved a new intraday record high of 7,147.78 on April 23. This move appears to be pricing in a durable resolution. Several factors argue against that outcome:

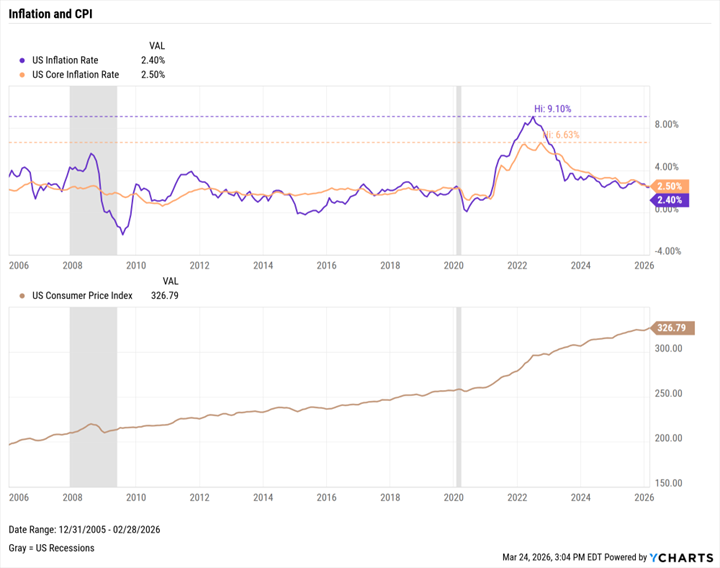

· March CPI came in at 3.3% YoY — the highest print in two years —indicating conflict-driven cost pressures are already flowing through toconsumers.

· The Trump administration's rhetoric and on going blockade are structurally inconsistent with the rapid normalization that current equity valuations appear to reflect.

· The U.S. blockade of Iranian ports continues to suppress Iranian export capacity independent of cease-fire status.

· Damage to regional shipping infrastructure, Oil & Gas production facilities, and Strait of Hormuz bottlenecks will take months, and potentiallly years, to fully resolve, even if active hostilities end tomorrow.

· Historical precedent is instructive: the 1991 Gulf War produced energy market dislocations that persisted well beyond the end of active combat, driven by infrastructure reconstruction timelines and sustained risk premia.

The cease-fire rally may prove premature. Even an immediate end to hostilities would leaves structural supply chain disruptions and inflationary damage that may take considerable time to unwind. Higher costs will be passed on to consumers, sustaining the persistent inflation the Fed has battled since 2020, a head wind for both economic demand and asset valuations that investors should not underestimate.

Airlines: Fuel Shock Accelerates Structural Stress

Jet fuel costs have surged from approximately $2.50/gallon pre-conflict to $4.23/gallon at majors. U.S. hubs, a 69% increase. For an industry where fuel typically represents over25% of operating costs, this is a significant shock to their margins.

Carrier-Level Stress

The impact is not uniform. Spirit Airlines, which has filed for bankruptcy twice since its attempted merger with JetBlue was blocked on antitrust grounds in 2022, is again in financial distress. Soaring fuel costs have overwhelmed the discount carrier's tight margins. The Trump administration is reportedly in discussions about a rescue package, which could take the form of extended financing or an outright government acquisition. Separately, merger conversations between American Airlines and United Airlines re-emerged then quickly faded, reflecting the industry's appetite for capacity rationalization in a sustained high-cost environment. JetBlue is also facing mounting solvency concerns, even as their CEO ruled out bankruptcy this year.

Operational Responses

Major carriers are hiking surcharges and cutting less profitable midweek routes to concentrate capacity on higher-yield segments. These measures partially offset cost increases but do not resolve them. American Airlines alone projects fuel costs could rise by $4 billion this year, pressuring margins in an already thin-margin industry.

The discount carrier model – built on high utilization, low yields, and minimal ancillary costs –faces structural headwinds if fuel remains elevated. Further consolidation within the budget segment appears increasingly likely, regardless of how the conflict is resolved.

Anthropic Mythos: A New Cybersecurity Threat Landscape

Anthropic has disclosed the existence of Claude Mythos, an AI model described by the company as capable of “exploiting zero-day vulnerabilities in every major operating system and every major web browser when directed to do so.” The disclosure has prompted a broad defensive response: government intelligence agencies, financial institutions, and major technology firms are accelerating cybersecurity upgrades in its wake.

Anthropic noted thatit expects AI models with comparable offensive capabilities to be released morewidely within approximately 18 months, indicating that Mythos is an isolateddevelopment but as an early indicator of a broader shift in the cybersecurityindustry.

Project Glasswing

Rather than a commercial release, Anthropic has taken a controlled deployment approach under Project Glasswing, sharing Mythos access with approximately 40 organizations, including U.S.-based firms like Apple, Amazon, and Cisco. The stated purpose is to allow these firms to identify and fix vulnerabilities in their own systems before models with similar capabilities proliferate more broadly.

CrowdStrike and Palo Alto Networks are among the select Glasswing participants. Both companies' stocks rose following the announcement, supported by analyst upgrades and the elevated awareness of AI-enabled security threats. Their inclusion in the Glasswing cohort is important: it signals that Anthropic does not intend to compete directly in managed cybersecurity services, and it positions both firms to expand their AI-powered security portfolios with capabilities that peers do not yet have access to.

Risks to Monitor

Reports have emerged that unauthorized users have already gained access to Mythos, though there is no confirmed evidence of malicious use. The incident raises questions about the durability of controlled access as similar models become more widespread. Additionally, the near-exclusive U.S. composition of the Glasswing cohort may have geopolitical implications. However, this strategic advantage may narrow quickly if containment is compromised or if foreign actors develop comparable models ahead of the 18-month timeline Anthropic cited.

For enterprise technology buyers broadly, the Mythos disclosure functions as a wake up call for accelerated security investment, a dynamic that stands to benefit cybersecurity firms with established AI capabilities.

Conclusion

To conclude, markets are pricing in outcomes that neither the available data nor reasonable inference support. The cease-fire remains unresolved, oil is holding above $100/bbl, and inflation is re-accelerating. Considering these factors, the cease-fire equity rally appears premature. At the same time, the Mythos disclosure has permanently raised the baseline for enterprise cybersecurity requirements. Successfully navigating these structural shifts will be challenging for investors without a clear-eyed view of the gap between where markets are priced and where the fundamentals actually stand.

Disclosure: This piece is not intended as investment advice and has not been tailored to any specific individual's situation. It is for informational purposes only.